In a Nutshell: Interest rates stabilized in August, while most risk assets rebounded. The Federal Reserve is now ready to start cutting rates as the global economy looks poised to cool.

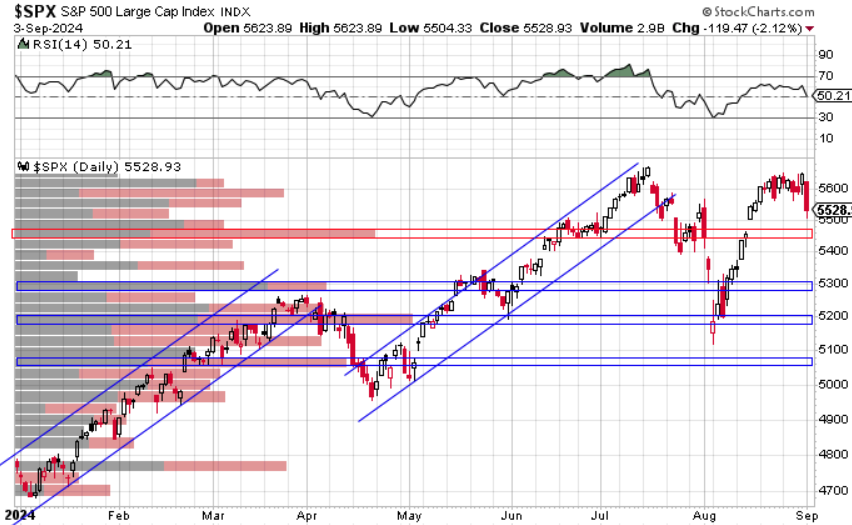

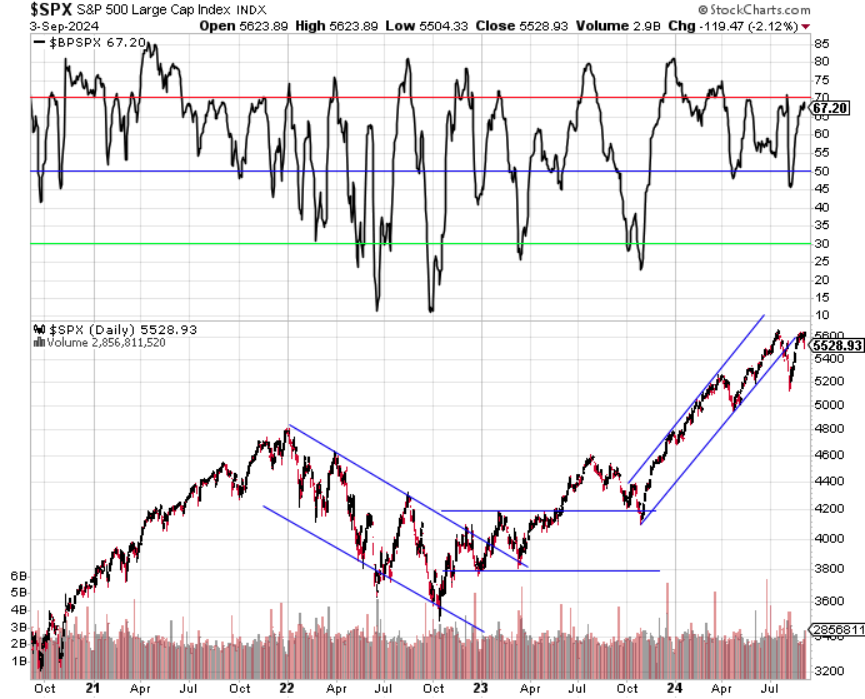

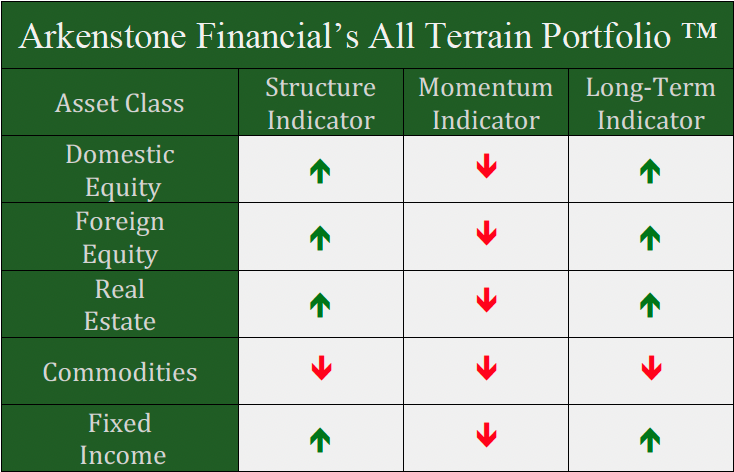

Domestic Equity: Big Bounce

The U.S. stock market found support where we were expecting it near the 5200 area. The rebound was quick, but didn’t lead to new all-time highs in the S&P 500, so stocks aren’t quite out of the woods yet. The biggest change in market structure since the recent selloff is that technology and growth stocks are lagging defensive or value stocks during this rebound. This is a departure from the first half of the year, where the rally was led almost exclusively by technology. This positioning change is likely due to an economic slow down in the U.S. through the third quarter and possibly through year end. Although growth looks to be slowing, it is not in a recessionary nature at this time. This rally will need time to show its strength as many of the lead stocks need a cool off and we enter what is typically a seasonally weak time of year for the stock market in September and into October. An ideal roadmap for closing the year at new highs would be holding the red box, but a more realistic goal given the previously mentioned headwinds would be trading above the August low through this seasonally weak period and into the fourth quarter.

We see a positive look on our participation model as it shows a healthy correction within a bull market.

Our sentiment indicator similarly shows a correction within a bull market.

The Federal Reserve officially made a policy pivot at their annual Jackson Hole meeting this past month. The Fed Chair, Powell, said “Now is time to cut,” referring to taking interest rates lower. The market has been asking for cuts for a while now so we’ll get to see if the pace at which the Fed cuts will be in alignment with expectations. At this time the interest rate market expects five 0.25% cuts by March of 2025, which is roughly a cut per month starting in September. Currently, the expectation is that the first cut in September will be anywhere from 0.25% to 0.5%.

Global Equity: Holding Up Great

We got a rebound from global equities in the blue box, as anticipated in last month’s commentary. This rebound eventually led to new all-time highs, which is something the U.S. market has yet to do. We favor global markets over the U.S. in the short term, as the global economic data looks a bit stronger than our domestic economic outlook. At this time the price action is saying the same thing.

India found support at the lower end of the channel during the early August sell off. Momentum is declining near previous highs so our longest standing position is on watch. India’s economic production appears to be slowing for the first time in a few years so we’ll keep an eye on this position.

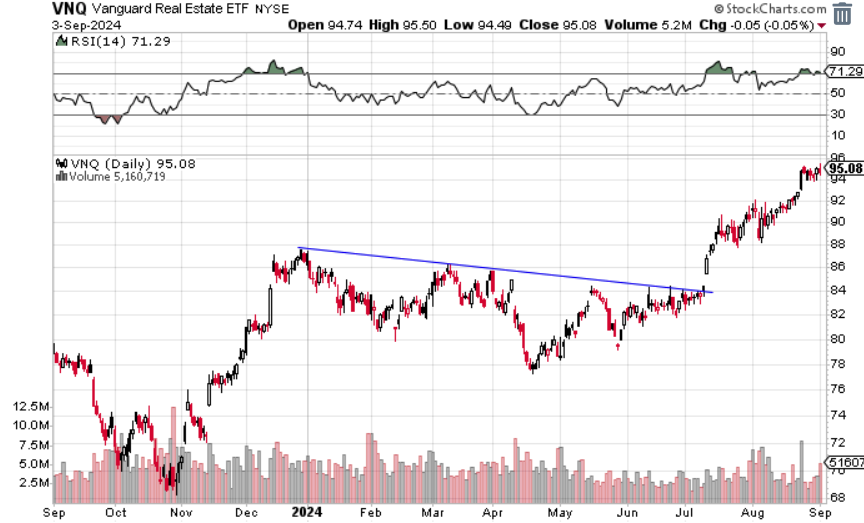

Real Estate: Still Not Stopping

Even after a blistering July, the real estate sector tacked another 4% on in August. Interest rates have been the key as rates have fallen, giving real estate a boost as well. Investors, despite the negative narrative surrounding the sector, have used real estate as a defensive position as the economy cools a bit in the third quarter.

To illustrate how far real estate had fallen out of favor with investors, we have a chart showing how real estate performed when compared to the stock market. As you can see below, real estate lagged the market significantly all year until the recent breakout – where it became an outperformer when compared to the stock market.

Commodities: On the Wrong Side of the Lines

Commodities traded flat in August and were rejected at a key level on their most recent bounce attempt. From an economic standpoint, commodities have traded as if the global economy is slowing. Commodities traded lower, along with interest rates, as a sign that demand may be slowing. This is good news for inflation, but slowing inflation at the expense of growth is a less than ideal scenario for the global economy.

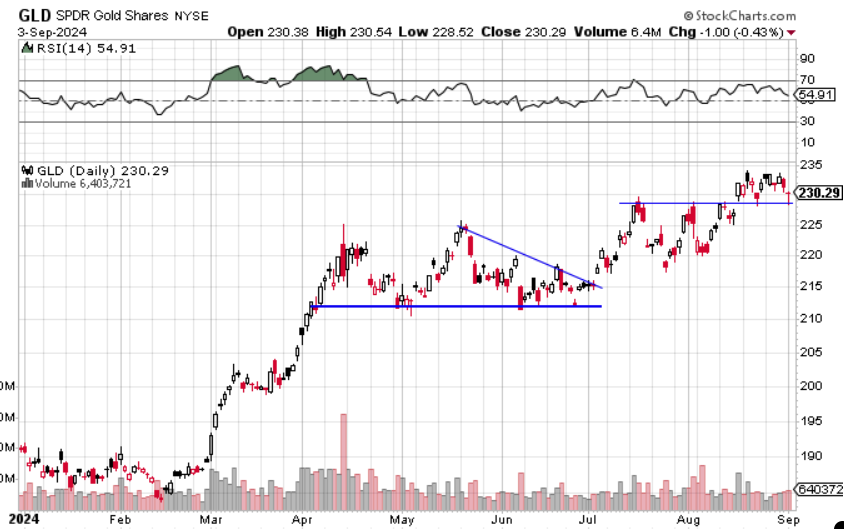

Gold knocked out new highs and modest gains in August and appears to be recharging near prior all-time highs. The outlook is straightforward from here: Holding the top blue line will be key in sending the yellow metal higher.

Fixed Income: Rates Stabilizing

Interest rates have found some support near one-year lows at 3.8% for the 10-year U.S. treasury interest rate. After such a huge move lower in July, it wouldn’t be surprising to see stability or a small move higher in rates from here. The second quarter GDP result was revised higher to 3.0% (annualized) while the Atlanta Fed is now casting a 2.1% result in the third quarter. Those two data points have moved in opposite directions over the past month, highlighting that we are likely in the midst of an economic slowdown (in the U.S.) but not one that is looking recessionary at this time. If rates plunge below the blue line below, that would indicate heightened fears for the economy by the bond market.

The interest rate market is still looking for five 0.25% rate cuts over the next year as evidenced by the forward looking two-year interest rate against the more current three-month interest rate. The Fed is now ready to cut rates, which will begin to start taking this difference to zero. Typically, the beginning of the rate cutting cycle is the end of the economic growth cycle. However, the post-Covid economic recovery has been unique, so the hope is that this cutting cycle is not like previous cycles. This time around, the Fed will attempt to lower interest rates to be less restrictive as the economy cools in an attempt to keep the current economic cycle going without a recession.

All Terrain Portfolio Update

Risk assets rebounded without triggering any red flags, according to our model. We took our technology-related risk down, but still maintain near-full allocation overall. We still carry about 20% in risk-averse, short-term treasuries less than three years in maturity that are paying interest in the 4-5.3% range. The economic data and outlook is tilting towards expansion, but slowing in the rate of expansion as we move further into 2024. Inflation, and by extension interest rates, will be the key driver for asset returns this year. We will follow our indicators as we wait for investment opportunities, but remain agile within our process as new data is presented.

Chart as of 8/31/24

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply