In a Nutshell: After an impressive rally, stocks crumbled to close out August. Interest rates, fueled by a resolute Federal Reserve, pushed higher.

Domestic Equity: Stalled Out

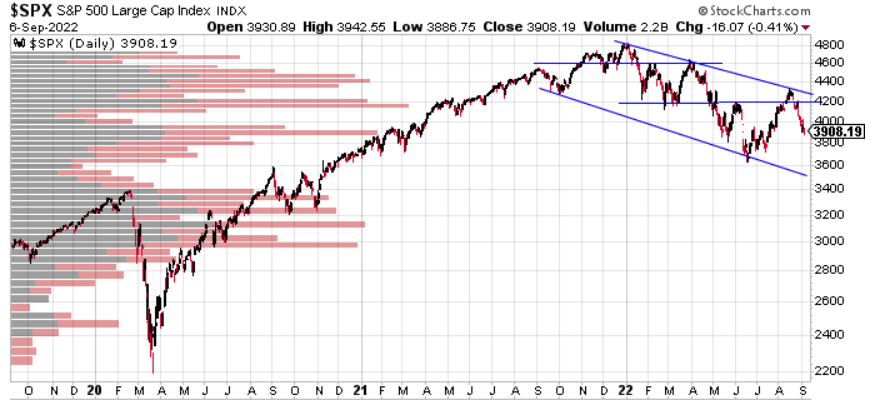

We pondered the question last month of “bear market rally or is the bottom in?” August’s price action seemed to favor the former. After an impressive 17% rally from the June lows, the S&P500 fell 9% in the final two weeks of August, finishing the month in the red. More importantly, we formed another significant local top that seems to align with prior local tops, forming a downtrend.

More evidence that we are still in the midst of a bear market can be found in our chart below, where stocks are making more new lows than highs. This latest rally barely pushed us above the zero (neutral) line before falling back into negative territory, meaning we still have more stocks making lows than highs.

To echo last month’s sentiment, we’ll need the worst performing stocks to show strength before we can consider changing our bearish stance. Smaller stocks, as shown below, are giving us a glimmer of hope. Rejected by their 2021 starting price, small caps are now on top of a down channel. If they can stay above the channel, we might be onto something positive for stocks. However, with more poor economic data ahead of us, our optimism remains muted.

The Federal Reserve did not have an interest rate meeting in August, so rates remain unchanged through the month. However, the Fed did have their annual Jackson Hole meeting where Jerome Powell addresses the state of the economy and monetary policy. Powell reiterated that the Fed is not backing off from throttling down the economy to fight inflation. He stated that he does not want to make the mistakes of policy makers in the 1970s and 1980s where they backed off too soon when fighting inflation. He directly stated interest rates will be higher for longer than we are used to seeing. The bond market is pricing in another 0.75% interest rate hike in September.

Global Equity: Weakness Is an Understatement

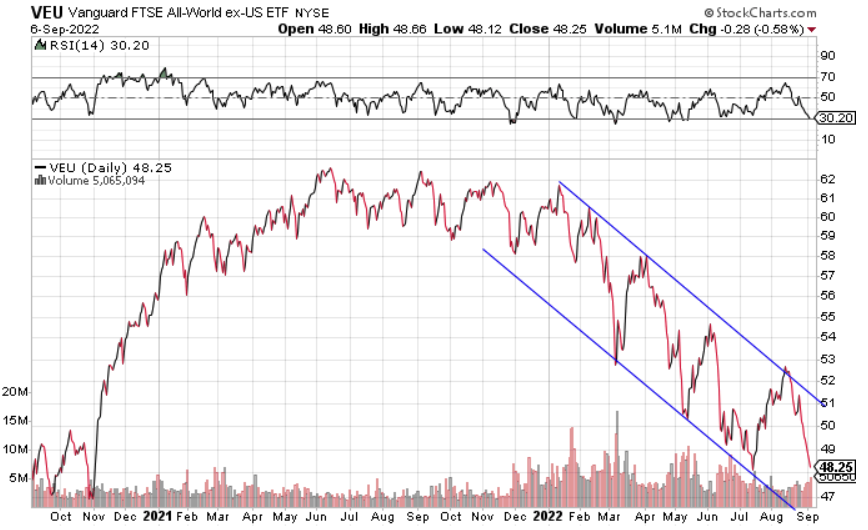

The global markets have displayed extraordinary weakness in 2022. The recent rally was only about half of the U.S. equity rally and in the end the entire rally was given back by the end of August. As you can see below, the steep downtrend couldn’t even be shaken on the last rally. There are a lot of reasons for this weakness as the U.S. Dollar’s incredible strength has put enormous amounts of pressure on global currencies and their economies. Additionally, a large contingency of the developed world, specifically Europe, is currently facing crushing energy costs and inflation, with no real means to combat these issues. Europe looks hard pressed to avoid a recession.

Real Estate: Sideways Churn Continues

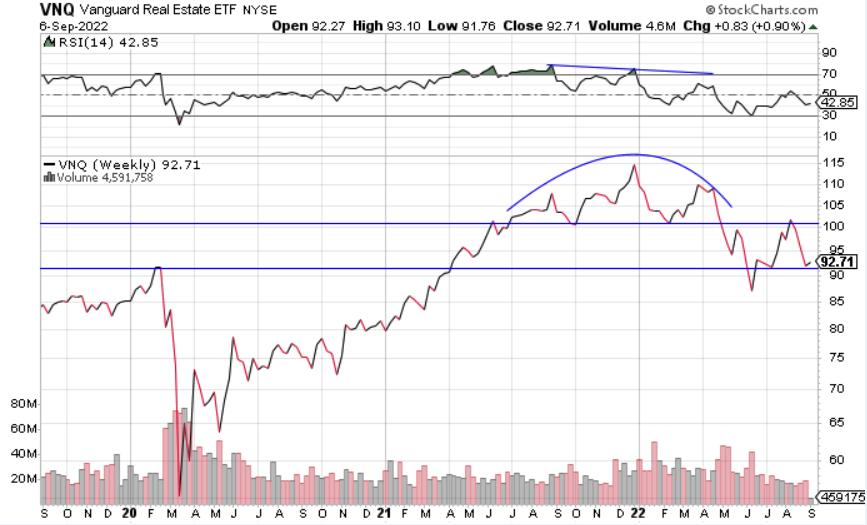

Real Estate rallied along with the rest of the market to start the month of August. The rally ultimately failed at a key spot, sending the sector lower for the month. As you can see from the chart below we are well below previous high water marks, but have been ping-ponging back and forth between support and resistance for the past four months. This type of consolidating price action should resolve one way or another. Given the current trend and the forward looking economic data, we’ll be looking for more downside.

Commodities: Have Commodities Peaked?

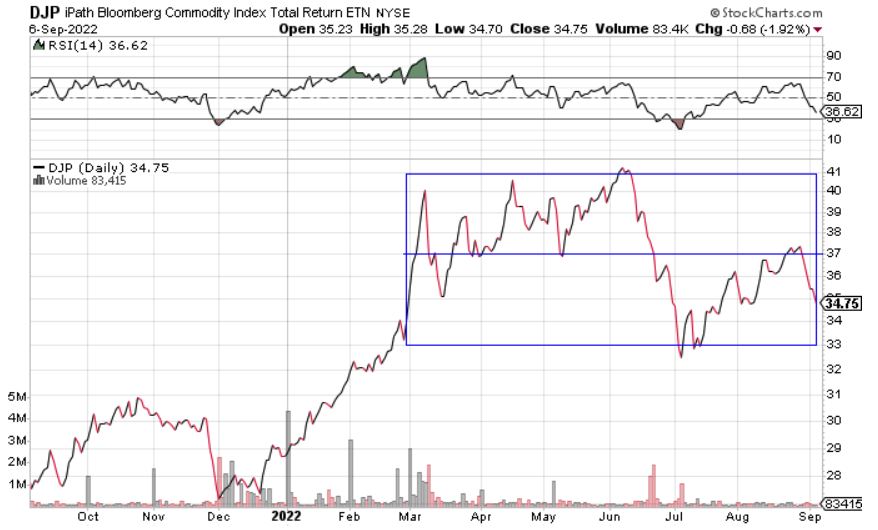

We’ve documented the incredible rally in commodities over the past two years, and the rising inflation that has accompanied it. But over the last seven months, commodities in general look to be topping. As shown below, commodities have traded within the box shown for most of 2022. More recently, over the past three months prices have traded in the bottom half of this box, well below previous highs. A break below the bottom of the box would all but confirm commodities have rolled over.

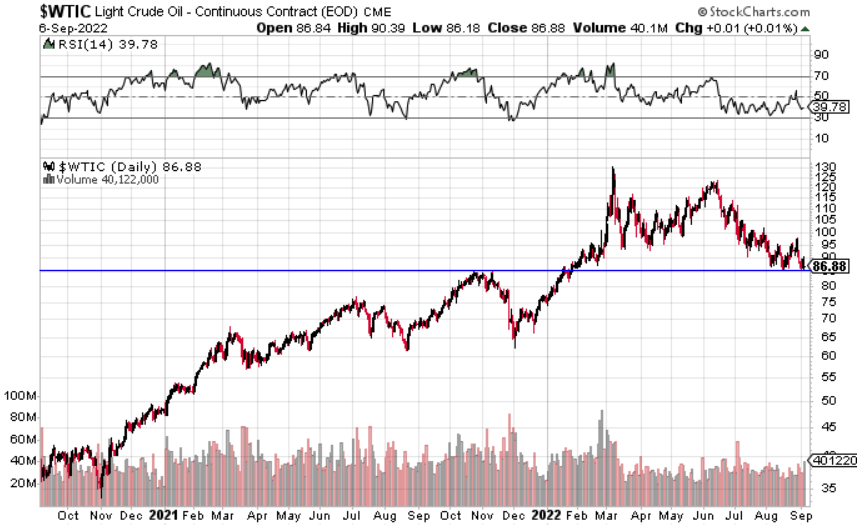

Oil has been a great proxy to follow commodities broadly. You can see below that oil is down about 34% from its March peak and is at a critical juncture. This recent price action has been good for consumers at the gas pump, but ultimately a bad sign for the global economy, showing reduced overall demand.

Fixed Income: The Fed Sent Rates Higher

Interest rates went ripping higher in August after the Federal Reserve Chairman Powell’s annual Jackson Hole speech. You can see below the brief breakdown from the 3% level on the 30 year U.S. treasury yield. From there rates went on to make new highs for 2022.

Not only were new high marks made for interest rates, the high from 2018 is now in sight. Breaking above the 3.5% level may indicate a long term regime change for interest rates, meaning they could be higher for longer. As mentioned in our equity section above, this type of interest rate movement is likely what Chair Powell was looking for after his recent speech. Higher interest rates will likely slow inflation and the economy.

All Terrain Portfolio Update

Our signals and indicators continued to rotate out of risk assets, as we now carry over 94% cash and short term notes in the All Terrain Portfolio. Despite the wide ranging potential investment exposures allowed by our model, there are very few investment options that fit our criteria currently. We will continue to wait for investment opportunities, and in the meantime, follow our indicators and process to adjust risk as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- Rising Rates Push All Assets Lower - May 10, 2024

- Gold, Stocks Make New Highs - April 5, 2024

- No Pullbacks, Stocks March Higher - March 8, 2024

Leave a Reply