In a Nutshell: Interest rates continue to rise at a blistering pace, hitting levels not seen in over a decade. Stocks and commodities across the globe fell, making new lows for 2022.

Domestic Equity: New Lows

Stocks closed the third quarter at the lowest levels of the year, down another 8% in September. The S&P 500 has now fallen 16% in the last 45 days, taking the index down 24% for 2022. A relief rally is to be expected given this large of a move over the last month and a half, but we’d expect the downward trend to continue over the coming months. Economic data continues to look weak well into next year, likely limiting any stock rallies.

A check in on our stock market strength indicator below shows we are in deeply negative territory. This indicates we have more stocks making low marks than high. Until we see any sustained time in positive territory, this is a bear market for stocks.

The Federal Reserve raised interest rates by 0.75% in September. Fed president Jay Powell doubled down on the Fed’s resolute stance in fighting inflation. He reiterated interest rates will be higher for longer than we are used to seeing. He even mentioned that the economy may have to go through some “pain” as a result of high interest rates. There seems to be no changeup to accommodative monetary policy in sight from the Federal Reserve. There is no Federal Reserve meeting in October, but the bond market is pricing in another 0.75% interest rate hike in November.

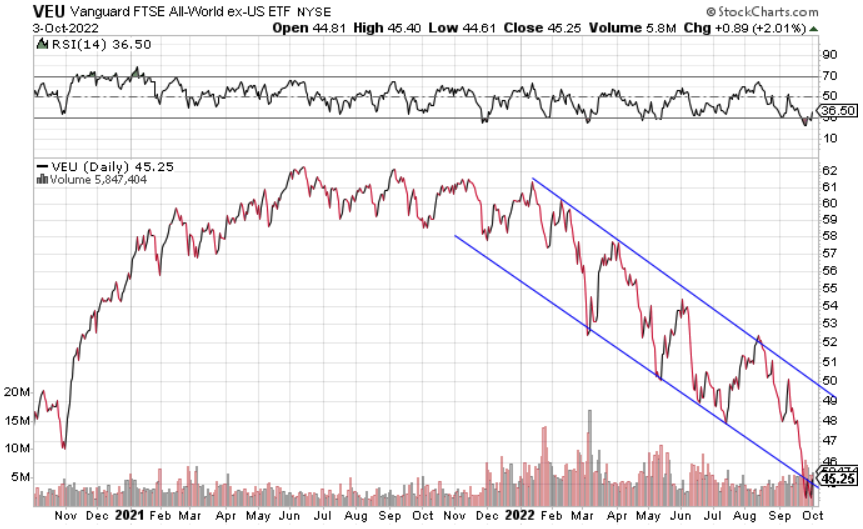

Global Equity: Total Collapse

Global markets fell 8% in September, making new lows on the year. Global stocks have been so bad in 2022 that this index now has a negative return going back to the start of 2018. Most global currencies are weakening against the dollar, while inflation runs rampant. Economic growth prospects look bleak across the globe well into 2023. It could be a while until global stocks are worth owning.

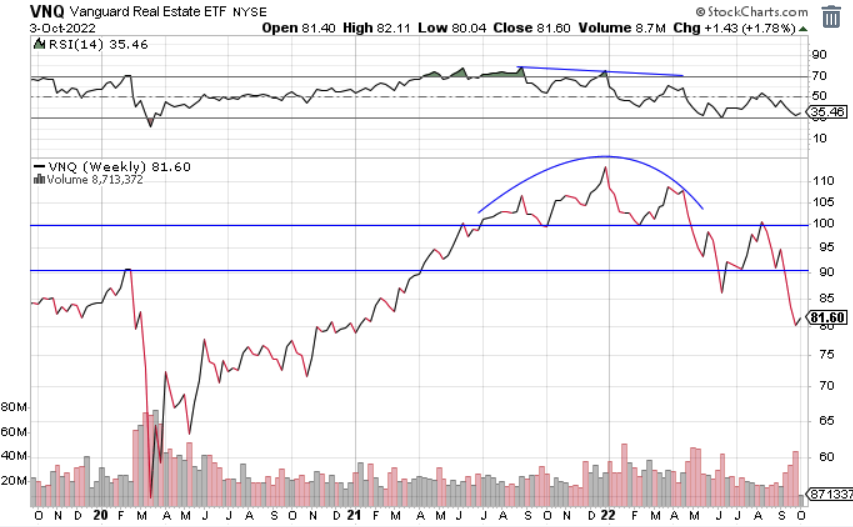

Real Estate: The Next Leg Down

Real estate closed September making new lows for the year, like just about every other asset class. While real estate showed some resiliency over the summer months, and slightly outperformed stocks, rising interest rates ultimately sent real estate lower. The national average for the 30-year mortgage clipped 7% briefly, more than doubling the rate from a year ago. Real estate prices, especially non-residential, can be influenced by other factors other than interest rates, but those factors hardly matter because of the pace that interest rates are increasing. Real estate won’t be worth owning until rates stabilize or flatten out.

Commodities: Hanging On, but Barely

Commodities closed out the month of September down 7%. The positive observation from commodities over the past month was that they did not take out the June lows. However, the sector is holding on to the bull case by a thread. You can see the two major trend lines since the summer of 2020 and the Russian incursion have been broken. Falling out of the blue box would be the final straw.

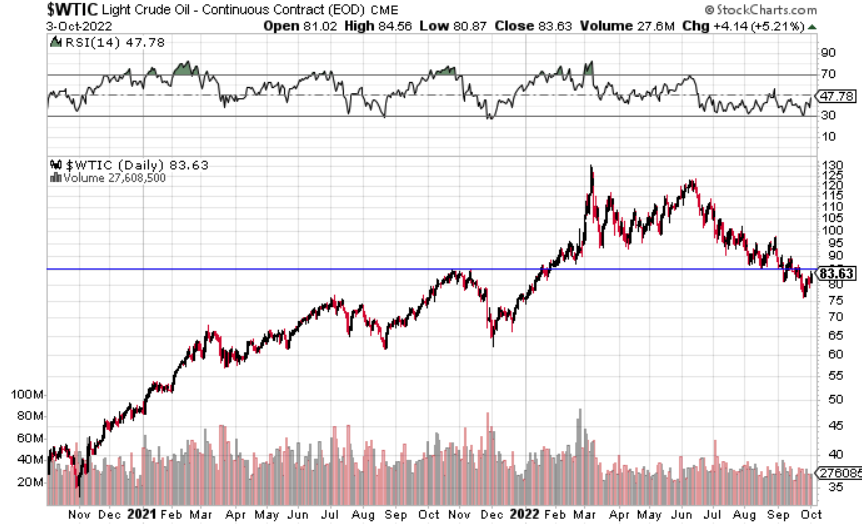

Oil is telling a similar story as it is now trading below the key high level that preceded the Russian conflict.

Aside from food, just about every commodity price is down significantly over the past 4 months. How bad has it been for commodities lately? As the small blue line in the 2022 portion of the chart below indicates, stocks have actually outperformed commodities so far in the second half of the year. This is in spite of stocks trading lower over that time period. This weakness in commodities may help slow inflation, but the byproduct is a slowing economy, globally.

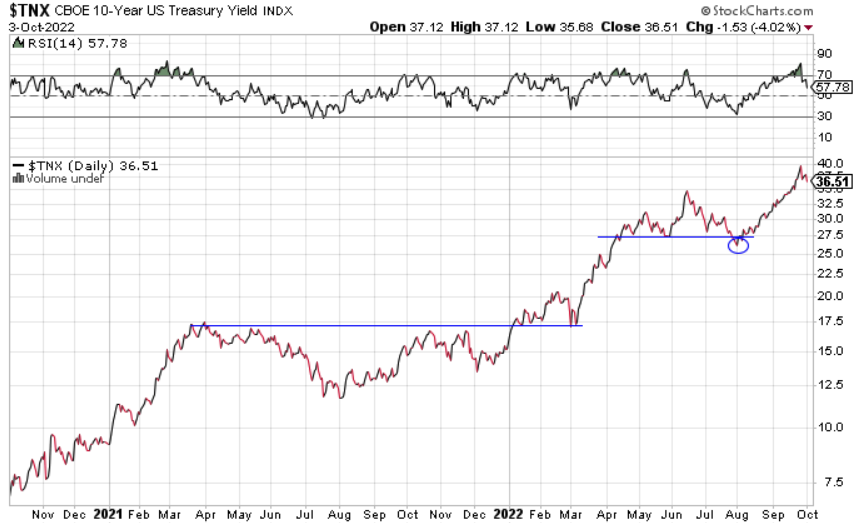

Fixed Income: Rates Explode Higher

The lead story in the investment markets over the past few months has been how fast interest rates are increasing. The total move in the U.S. 10-year treasury bond over the past few months was from 2.6% to a brief clip of 4%, a 54% increase in just a little under two months. The huge move in rates means bond prices have fallen significantly. You can see that big move below.

Zooming out on the 30-year U.S. treasury interest rate, you’ll see that the move from the 2020 until now is the largest nominal move we’ve seen over the last 40 years.

The result has been chaos across just about all investable markets. Many currencies, stock markets, bond markets and commodities have experienced 20 to 30% drawdowns. To underscore this point even further, when you analyze stock and bond data going back to 1928, you’ll only find five years when both stocks and U.S. treasury bonds are down in the same year. Over that same time period there has never been a full calendar year when both stocks and bonds were down by more than 10%. So far in 2022, stocks are down 24% and bonds are down 17%. This is a truly unprecedented pace in a historically bad way. Until interest rates stabilize, the entire macro investment landscape will be incredibly harsh on risk assets.

All Terrain Portfolio Update

Our signals and indicators dictated that we remove the final small remaining risk assets. We now carry 100% cash and short term notes in the All Terrain Portfolio. We will continue to exclusively hold safe positions that pay interest until the investment backdrop improves for risk assets. Despite the wide ranging potential investment exposures allowed by our model, there are very few investment options that fit our criteria currently. We will continue to wait for investment opportunities, and in the meantime, follow our indicators and process to adjust risk as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply