- The Federal Reserve increased interest rates in September.

- Rising rates put pressure on bond prices.

- Commodities rally.

- Global equities continue to struggle.

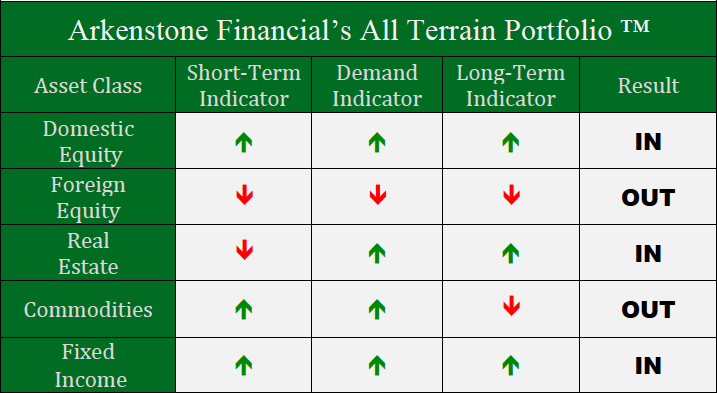

Domestic Equity

U.S. stocks were mostly flat for the month of September. Despite a lackluster month, U.S. equities are still strong relative to global stocks. Healthcare was a major leader this past month, racking up another 3% gain on top of a nearly 10% run over the last few months. One area of concern in U.S. markets is the lack of participation of financials (banks) in this most recent rally. It’s odd to see banks sit out a rally, especially with interest rates rising — a key contributor to bank profit margins. This could be a product of a healthy investment environment with banks waiting their turn within broader sector rotation, however, it’s worth noting this type of behavior by banks occurred prior to the Great Recession, so we will continue monitoring this situation.

The Federal Reserve raised rates by one quarter of one percent at the end of September. The move was expected by markets, and the Fed has signaled intent to raise again this year. Currently markets have an 81% chance of another rate hike in December.

Global Equity

Global equity gained roughly 2.5% in September. However, zooming out on the timeline reveals that this was likely just a short-term, counter-trend rally within a broader down trend. Developed and emerging markets have flirted with breaking out of their rut, but still lack the momentum to do so. Falling local currencies, along with increases in trade costs, have put a lot of pressure on equities outside the U.S. Right now stocks outside of the U.S. are worth avoiding.

Real Estate

Real estate was down this past month. A combination of factors triggered this pull back, one of which was the price resistance we mentioned in previous months. Real estate could not hold the price point it approached in September, and consequently fell, and rising interest rates will put additional pressure on bond proxies like real estate. Real estate is frequently attractive because of the high yields, however, with fixed income yields climbing, real estates loses some relative value. Lastly, we typically see a lot of selling in high yield securities (like real estate) at the end of calendar quarters, when investors rush into these products in time to qualify for the dividends, and sell upon receipt of the dividend.

Commodities

Commodities took off in September, posting a 6% gain for the month. We mentioned last month that divergence between price and momentum has been building to a point where a local bottom was in the making. That’s exactly what came to fruition as the commodities slide came to a halt by mid-month, followed by a very strong rally to close the month. It was great to see some strength in a sector that has been so beaten up as of late. If commodities can continue their strength and break through a years-long price resistance, a long-term positive thesis will be in play.

Fixed Income

Just about all bonds — government and corporate — lost value in September. We’ve mentioned before that bonds will lose value when interest rates increase. The high probability of the end September rate hike triggered selling for the entire month. Long term treasury bonds broke down below key support as interest rates broke through, at least temporarily, resistance that goes back decades. If the bond market comes to accept that rates will continue to increase, more selling will continue. It’s not all bad news though, as all of this selling will ultimately shift new dollars to alternate investments. Stocks, both global and domestic, could be the benefactors.

All Terrain Portfolio Update

The All Terrain Portfolio carries its cautious investment approach into October — a notoriously volatile month. Although we have seen positive action in U.S. markets as of late, we will continue to closely monitor all sectors with our various indicators, key support, and technical levels.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- Gold, Stocks Make New Highs - April 5, 2024

- No Pullbacks, Stocks March Higher - March 8, 2024

- U.S. Stocks Hit New Highs - February 9, 2024

Leave a Reply