In a Nutshell: All asset classes aside from bonds rallied to close the year out. As the book is closed for 2020, investors will eye economic recovery and the fiscal policy that will support it.

Domestic Equity: Rotation Does a Market Good

U.S. stocks finished the year strong and completed a monster rally off of the March lows. Although technology stocks pulled us out of the depths of the sell off, more cyclically sensitive stocks have now taken over as the optimism of reopening the economy increases. Below, we see the relationship of small cap stocks and large cap stocks. When the trend is up, small cap stocks are leading and the opposite is true as well. Smaller stocks tend to be more cyclically sensitive and tend to do better than large stocks in times of economic expansion. Below, you can also see how small cap stocks lagged (as the economy slowed) for the last few years heading into 2020 and were decimated in the COVID-19 crisis. However, for the last three or four months, small cap stocks have led the way. Seeing the more economically sensitive stocks take over leadership for technology is a very positive sign going forward.

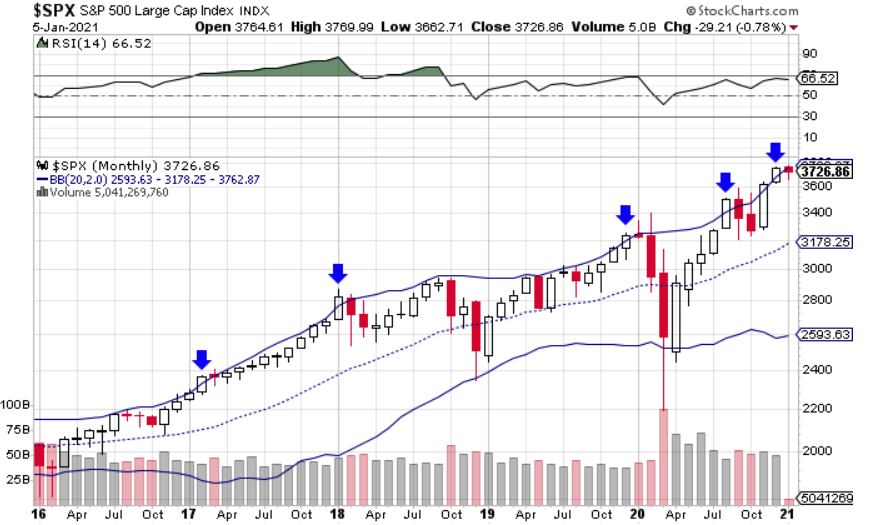

There is much to like about the stock market right now, but it may be due for a cool down. Below is a chart that shows how far stocks are stretched in one direction. For the last four years, anytime we’ve closed a month beyond the upper band, we see that at least the next month has been negative. While it is healthy for a hot market to take a breather, the last few instances led to rather swift and significant drawdowns. At the very least, investors may want to reset expectations for the beginning of the year.

The Federal Reserve met in December and reiterated their desire to keep interest rates at zero and implored Congress to work toward fiscal support for the economy. The Fed seems dead set on passing the policy baton to Congress and seems to be indicating that the monetary policy of the last few decades is changing.

Global Equity: Leading the Globe

Emerging markets (EM) continue a very impressive short term run. Blasting through previous highs to make a new all time high for the first time in two years, EMs are now leading all global stocks higher.

The chart below shows the relationship with EMs and U.S. stocks. For most of the 2010s, U.S. stocks have been the leader here, hence the downward trend overall. However, for the last two quarters EMs have outpaced U.S. stocks. With a continued weakening of the U.S. dollar, this outperformance may be a key theme in 2021.

Real Estate: Closing 2020 Out at a Loss

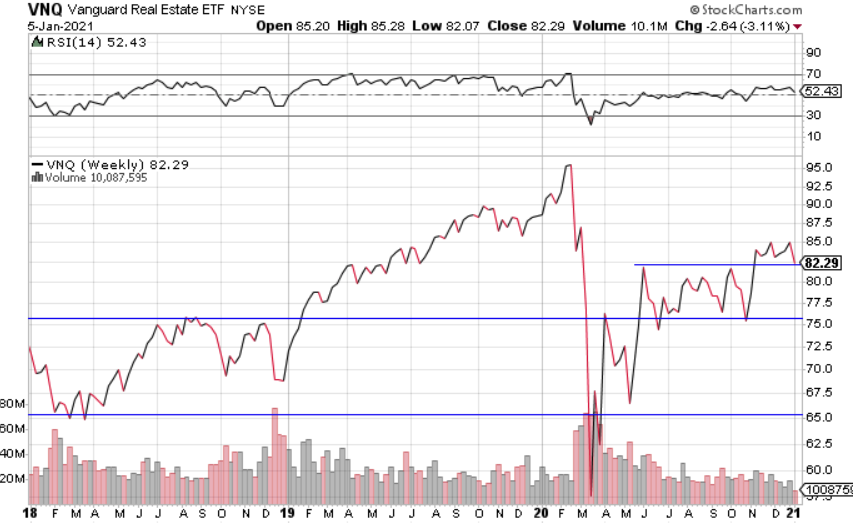

Real Estate had another meandering month to close out 2020, and continues to lag the broader equity market on a relative basis. On the positive side, real estate held its short term support from the past few months, which is important for future price appreciation. Until we see more positive trends in this sector we’ll keep our position small.

Commodities: Sleeping Giant Awakening?

Gold has been in hibernation mode for the most of the past five months, but may have broken out again at the end of 2020. Gold had a huge year this year, but spent most of the last half of the year consolidating large gains from earlier in the year. In what appears to be a natural breather within the context of the bull market trend, gold may be primed for another move up. Seasonal trends may assist as well, as the last seven Januaries have been positive for gold with an average return of 4.7%

Fixed Income: Rates on Firm Ground, Looking to Go Higher

Interest rates are down significantly on the year, but rallied strongly in the back half of the year on hopes of economic reopening. With the 10-year note sporting an interest rate on the good side of the 0.9% support level, longer-term rates, which factor in future growth and inflation more sensitively, now are approaching a very long-term resistance level.

The 30-year treasury interest rate is now at 1.7% and climbing. Breaking through the long-term resistance (blue line) around the 1.8% level would indicate the bond markets think economic growth and recovery has arrived. As long as rates are rising, bonds will be a drag on traditional portfolios.

All Terrain Portfolio Update

The All Terrain Portfolio has continued to add additional risk assets small in size and narrow in focus. We continue to scale into our positions methodically over time in order to better absorb the current highly volatile investment environment. We will continue to follow our methodology and indicators to find buying opportunities and manage risk.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply