In a Nutshell: U.S. stocks had an incredible month in November. Meanwhile, a rising dollar and, by extension interest rates, have put pressure on just about every other investment sector.

Domestic Equity: Stocks Pop, Again

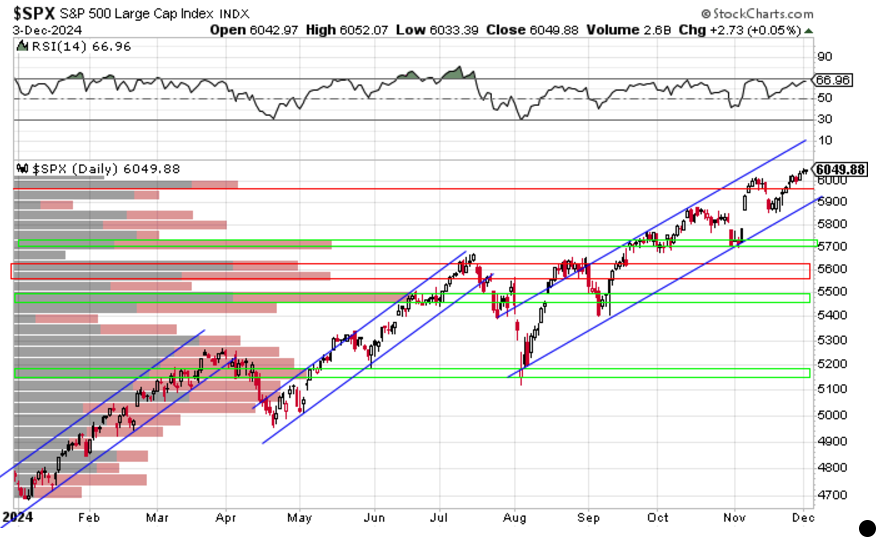

U.S. stocks made fresh all-time highs in November. We mentioned last month that stocks looked coiled and ready to run higher as we entered the month. That’s exactly what we saw as the 5700 level on the S&P 500 was backtested and then used as a springboard higher. The economy remains strong and continues to push stocks higher. Looking at the blue channel that the stock market is currently residing in, there appears to be a little more upside into year end. We’d like to see the 6000 price level hold on a test before sending the market higher.

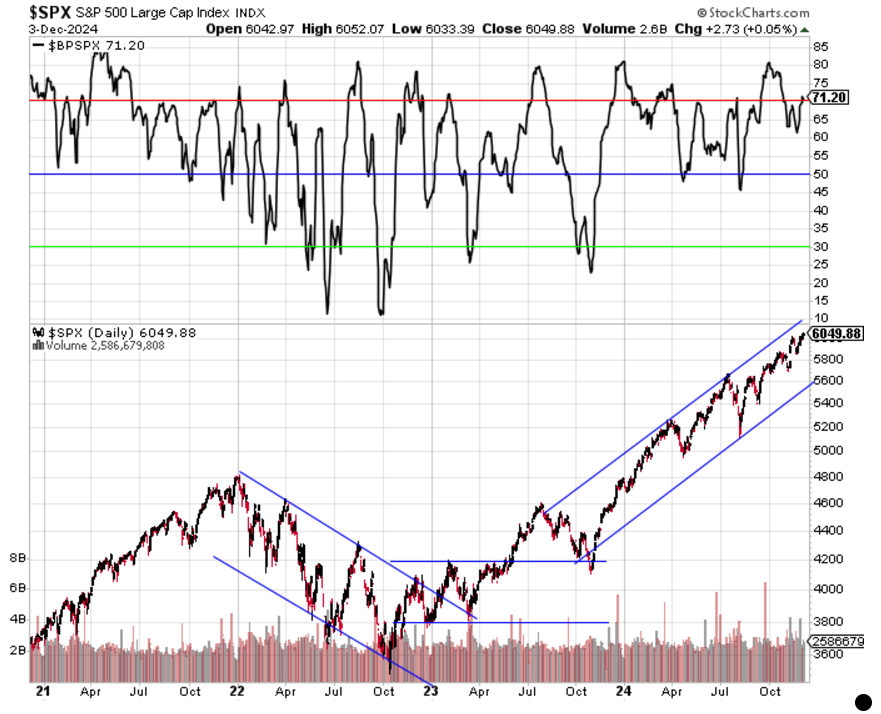

Again, our participation model has consistently stayed in bull market territory, with another round trip from the blue line (neutral) at the beginning of the month to oversold (red) by the end. This is textbook bull market behavior.

Our sentiment indicator similarly shows a bull market that cooled enough by the beginning of the month to head back to the redline. Some cooling may be needed from here to head higher.

The early November Fed meeting included another interest rate cut of 0.25%, taking rates down to 4.5%. The interest rate market is currently giving a 70% chance of another cut in December. Whether the next cut happens in December or the following month, it appears the market only expects one more cut for the next year or so. The economy has stayed strong and inflation has been rising slightly again, so it would not be surprising for the Fed to pause rate cuts to see if this current bout of inflation will subside. For now, short-term rates look pretty stable for the next year or so.

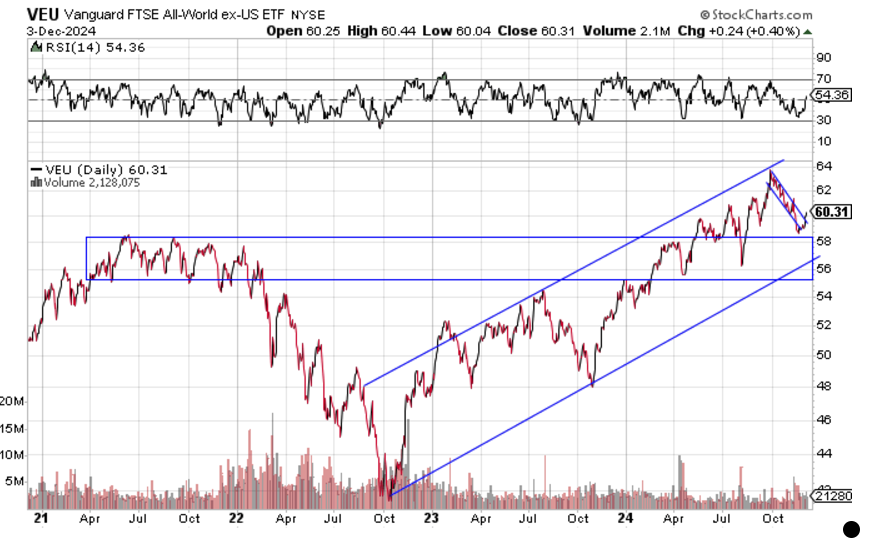

Global Equity: Still Can’t Get Footing

Although U.S. stocks stole the headlines in November, what was lost in the excitement was that just about everywhere outside the U.S., stocks have been declining. We still have not seen a critical break in global stocks as the big blue box is still holding, but we are getting very close. If you squint, it looks like global stocks are trying to break out of the blue down channel from the past month. We’ll need to see more of that price action for us to hold the position. The global economy is cooling a bit and inflation is rising which isn’t a great combination. Policy is a new headwind as the Trump presidential victory has put tariffs back in play for many global economies.

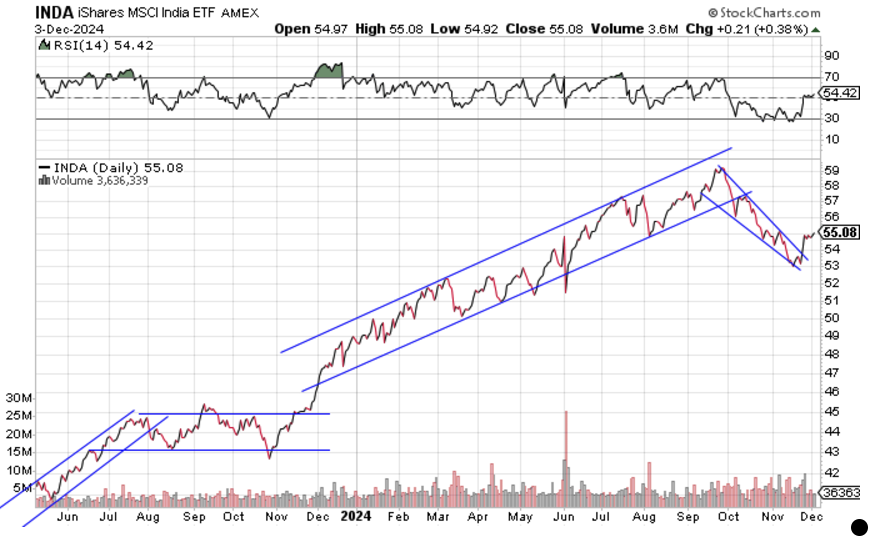

India was not immune from weak global stock performance, but hopefully we are seeing a breakout from a larger than normal pullback and consolidation there. We’ll need to see quite a bit of strength from this point forward to assume the uptrend has resumed.

Real Estate: Ready to Run Again?

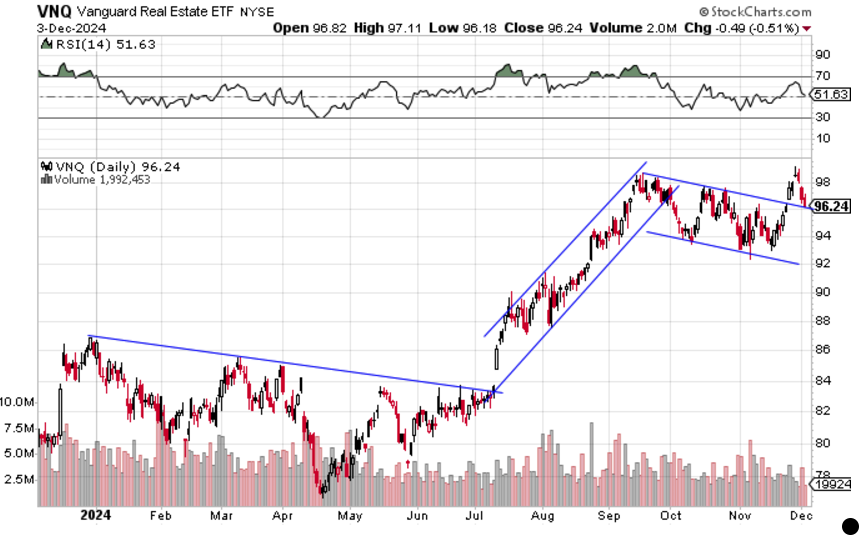

Real estate bounced back with a positive return in November. We mentioned last month that the sector seemed to be consolidating and would likely resolve by moving higher. We eventually got that move higher, with the sector making new high marks for the year this past month. The big driver of the move was interest rates. Rates finally backed off and rolled over, creating some relief in real estate. It’s worth watching from here as the price is retesting the consolidation zone. This is happening while interest rates are trading at the low end of their range. Those two positions are at critical points and one or the other will have to go higher, but likely they won’t both head higher together.

Commodities: Fast Then Slow

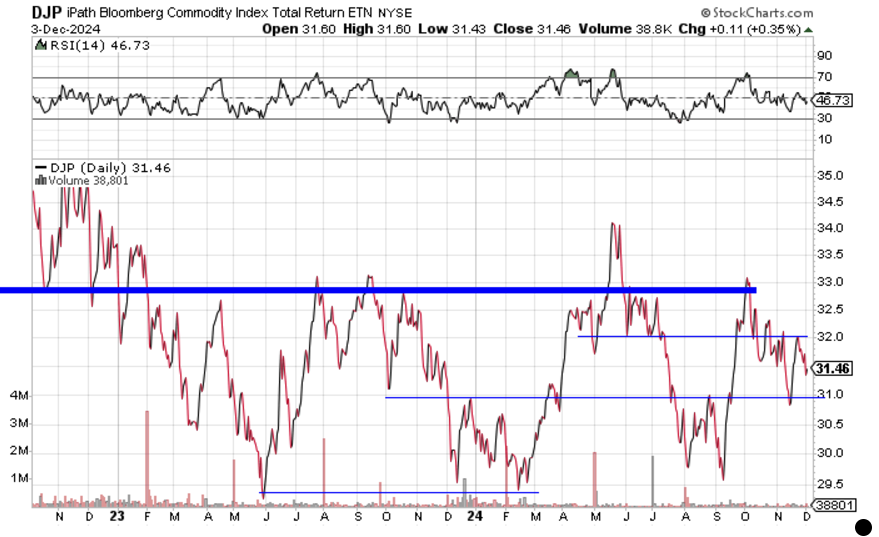

There isn’t much to update in the commodities sector. Price continues to be stuck between critical zones even with inflation perking up a bit. As we’ve seen over the past few years, most of the big moves have happened suddenly, followed by periods of stagnation. However, this most recent slow period has been part of a downtrend, so we’ll need a trend reversal to hold this position much longer.

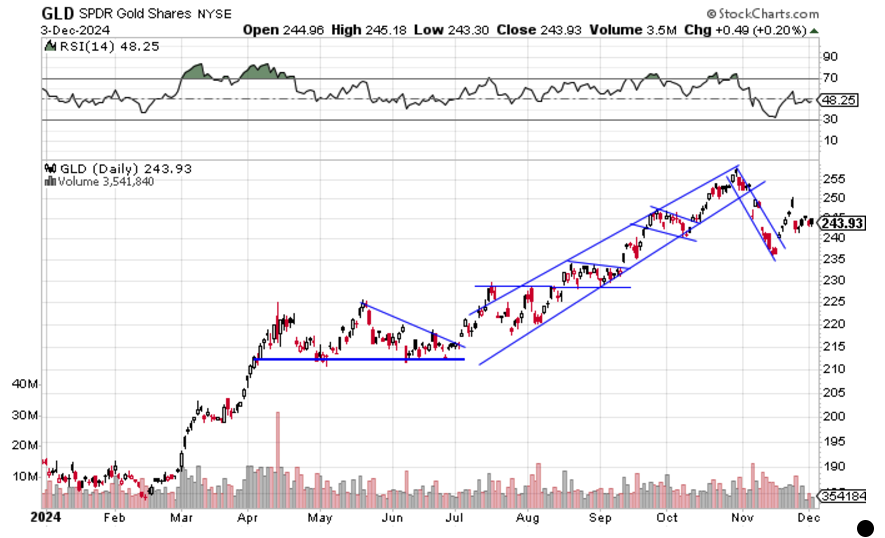

We’ve noted strength all year for gold. That strength came to a screeching halt in November as gold had its worst month of the year. To add insult to injury it is looking like a medium term trend has broken for gold in the process. This weakness occurred with a strengthening dollar that seems to be fueled by global inflation, a trend resulting in weakening global currencies weakening against the dollar. If the dollar keeps going up, and gold breaks the November lows, we may be seeing the early stages of a longer-term downtrend.

Fixed Income: Finally Some Relief

Interest rates continued to rip until about mid November before finally backing off around the equilibrium area that’s indicated below with the green box. As we mentioned last month, when the medium-to-long end of the yield curve (interest rates) is rising, that is going to put a lot of pressure on most investments. We continued to see that investment environment as nearly every investment sector was down last month aside from U.S. stocks. There is a lot to digest in the rates market as inflation is perking up again and the potential of new economic policy with new leadership in the Oval Office. Stability in the rates market would be a welcome sight regardless of direction, as interest rate volatility remains elevated, leading to big swings in asset prices.

The “Fed Yield Curve” (below) shows that the market thinks interest rate cuts by the Fed are effectively done. With one more cut of 0.25% expected in December, our chart below would move to roughly 0%, meaning no more cuts expected. The economy continues to hum along, and with inflation perking up again, the Fed would be wise to leave a few arrows in their proverbial quiver.

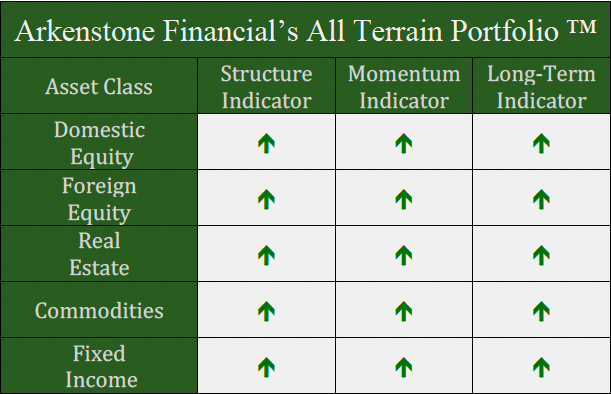

All Terrain Portfolio Update

The All Terrain Portfolio continues to remain at full allocation as we continue to tweak and adjust positioning for a rising rate and inflationary environment. We still carry about 20% in risk-averse, short-term treasuries less than three years in maturity that are paying interest in the 3.5-4.6% range. The economic data and outlook is tilting towards expansion as we approach 2025. Inflation and interest rates will be the key driver for asset returns as we close out the year. We will follow our indicators as we wait for investment opportunities, but remain agile within our process as new data is presented.

Chart as of 11/30/24

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply