In a Nutshell: U.S. stocks and gold had a great start to the year, making new all-time highs. Oil leads the commodities complex higher, stoking inflation fears again and pushing interest rates up.

Domestic Equity: Still Going Up

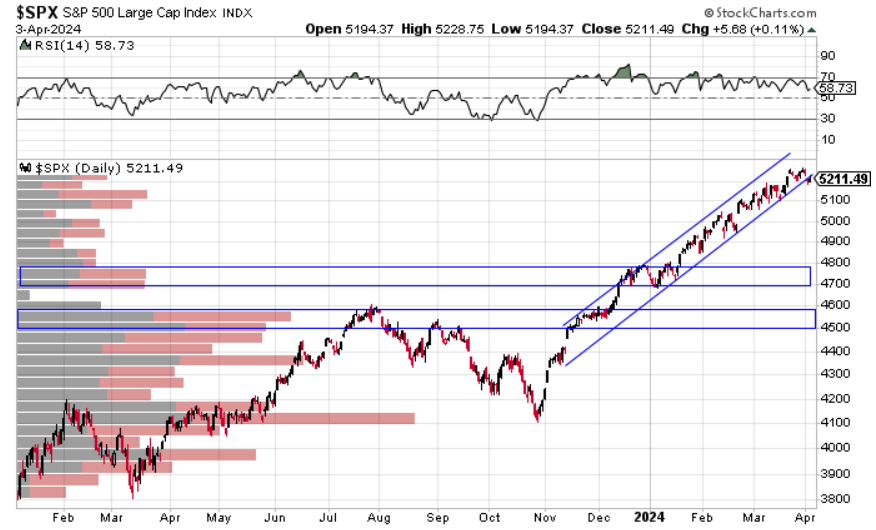

U.S. stocks enjoyed a strong start, up 10% to close the first quarter of the year. Stocks have marched higher for months now as economic data continues to be better than expected. The first quarter GDP estimates are now settling into the 2.5% range and most economists have made upward revisions, predicting 2% growth for the year. While that is positive for stocks, a healthy pullback would be a good thing to get new money into the market. You can see below that we are on the cusp of breaking this upward trading range we’ve enjoyed for the past four months. With the economy humming, we see any dips in the stock market as buying opportunities.

By far the most encouraging part of our recent rally is that the participation has been widespread, meaning most stocks have headed higher. We haven’t seen this type of bull market characteristic since the end of 2021. Big tech has taken a breather for the first time in the last year or so while broad participation has pushed prices up.

Sentiment is still pretty frothy, so seeing a cool off somewhere below the red line and above the blue line would be a long-term positive for the stock market.

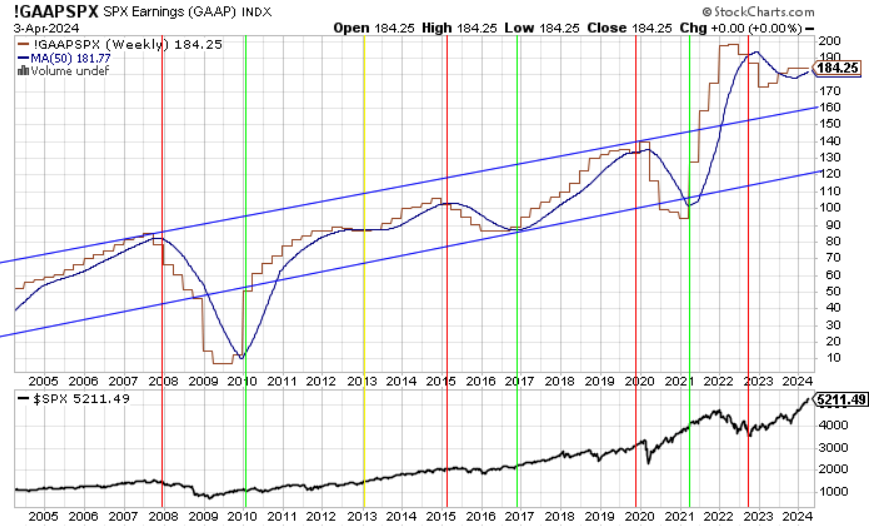

The first quarter of the year showed corporate profits continued to rebound and are trending in a positive direction again.

Interest rate policy remained at 5.25-5.5%. What’s interesting now in the interest rate market is that the combination of the Federal Reserve’s willingness to keep rates increased while risk assets rally higher (in anticipation of rates cuts, of course) is that the interest market has adjusted its expectations from a 1.5% point reduction in 2024 to 0.75% point reduction in just two months. The Fed, for now, seems intent to get inflation back to its 2% target before cutting rates, although recently Fed Chair Powell walked back the “need” to get inflation back to 2%. Until the stock market or economy cools, the Fed has little incentive to cut.

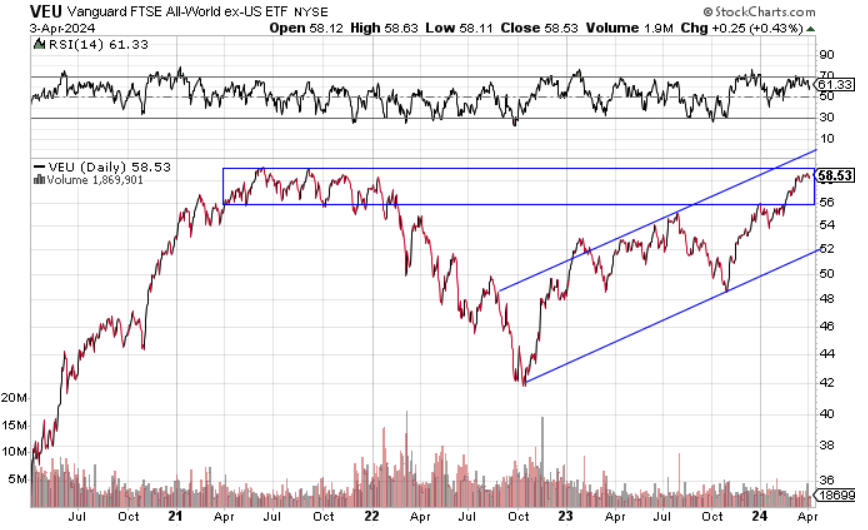

Global Equity: Going Strong

Global equities finished the first quarter strong, up nearly 10% to start the year. You’ll see the global index has run into some resistance in the blue box area, as we mentioned last month. There are still parts of the global economy that are trying to get their footing, but overall global growth looks very positive in the back half of 2024. While we may see some consolidating at these current price levels, we are expecting a good year overall for global equities.

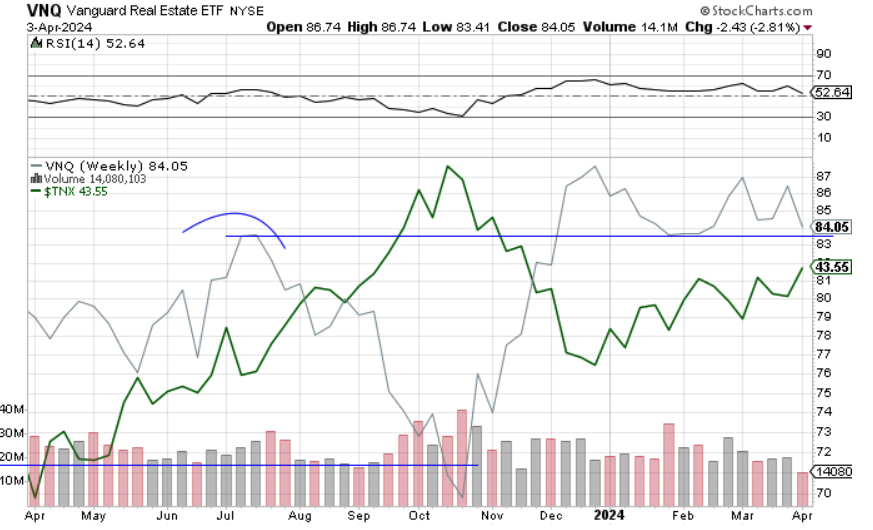

Real Estate: Interest Rates Are a Threat

Stocks have gotten off to a great start to the year, but real estate is a different story. The real estate sector finished the first quarter down about 2% on the year. While residential real estate has been stable to strong, much of the commercial real estate space has been weak. The broader problem for real estate is rising interest rates. You can see below real estate (gray) and interest rates (green) have been moving inversely for the past six months. With interest rates up to start the year, real estate is down. You’ll see in our fixed income section (below) that interest rates are on the cusp of breaking out higher to levels that put pressure on risk assets last fall. Real estate will be on a short leash for us.

Commodities: Is Inflation Back?

Commodities had a strong month in March as inflation has remained sticky. The biggest driver has been oil which is up about 24% to start the year. Oil pricing seeps into quite a few places in the economy so inflation will likely remain sticky at our current levels throughout 2024. Looking at the chart below, while we are still below the big blue line that has acted as resistance for the past 18 months, you can see the smaller blue lines showing that a reversal is in the works.

Gold went into orbit this past month as the precious metal blasted 12% higher on the month. You can see how incredible the move was as it sticks out even on the chart below looking back over 12 years. This is a huge move that will likely need a cool off, but this is an interesting development as gold has run higher while interest rates have also gone higher, breaking the traditional inverse relationship between the two. Gold is now outpacing the stock market to start the year and is one of our biggest positions.

Fixed Income: Is a Run Higher in the Works?

We mentioned last month that interest rates were looking like they wanted to run higher, and that they’ve done. You can see the well defined upward channel in blue below that is almost through the green box. The reason we highlight the green box is above it we saw a lot of pressure on risk assets. Last summer and into the fall we saw a 12% decline in stocks as interest rates rose from 4.4% to 5%. With inflation remaining sticky, along with higher expected GDP for the U.S. economy and recent hesitancy on future rate cuts by the Federal Reserve, it seems rates have the all clear to head upward. Risk assets may be a bit temperamental as rates rise.

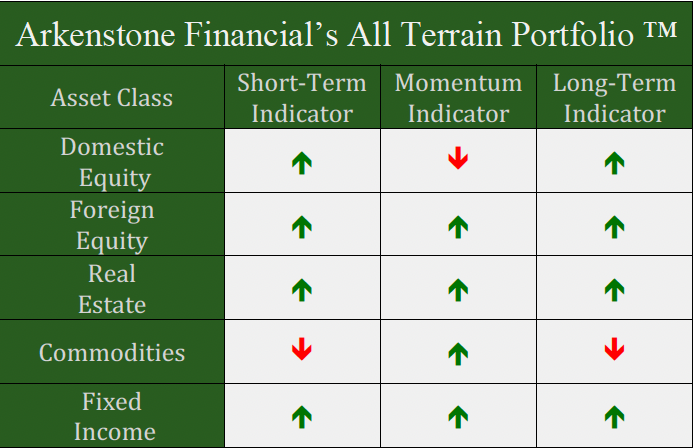

All Terrain Portfolio Update

Our model and indicators had us adding incremental risk into April, pushing the model near full investment. We still carry about 15% in risk-averse, short-term treasuries less than three years in maturity that are paying interest in the 5-5.45% range. We will be looking for pullbacks to add risk over the next couple of months to reach full investment as the current risk/reward for risk assets is low. The economic data and outlook now appear moderate to strong as we move further into 2024. We will follow our indicators as we wait for investment opportunities, but remain agile within our process as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

- Interest Rates Stabilize, Stocks Bounce - September 6, 2024

Leave a Reply