In a Nutshell: With the global economy moving steadily higher, stocks and interest rates rose across the globe. Stocks have lost some of their leaders from 2023, but are making up for it with broader participation. Interest rates look to remain higher for longer.

Domestic Equity: Are There Any Bears Left?

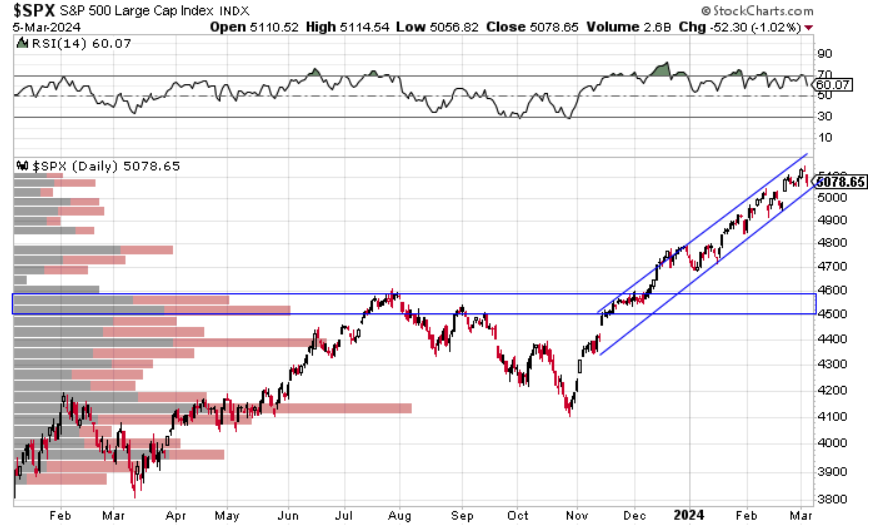

The U.S. stock market closed up 4% in February. Traditionally this is a weak month for stocks, however this past month was the best February return in over a decade. This is a continuation of a relentless move higher in stocks that has gone on for four months now. You can see in the chart below how U.S. stocks have maintained a steep and narrow channel higher for some time. The economy continues to perform better than most analysts project as the current Q1 GDP projection is roughly 2.5%. March tends to be a seasonally weak month for stocks, so we’ll watch for a breather.

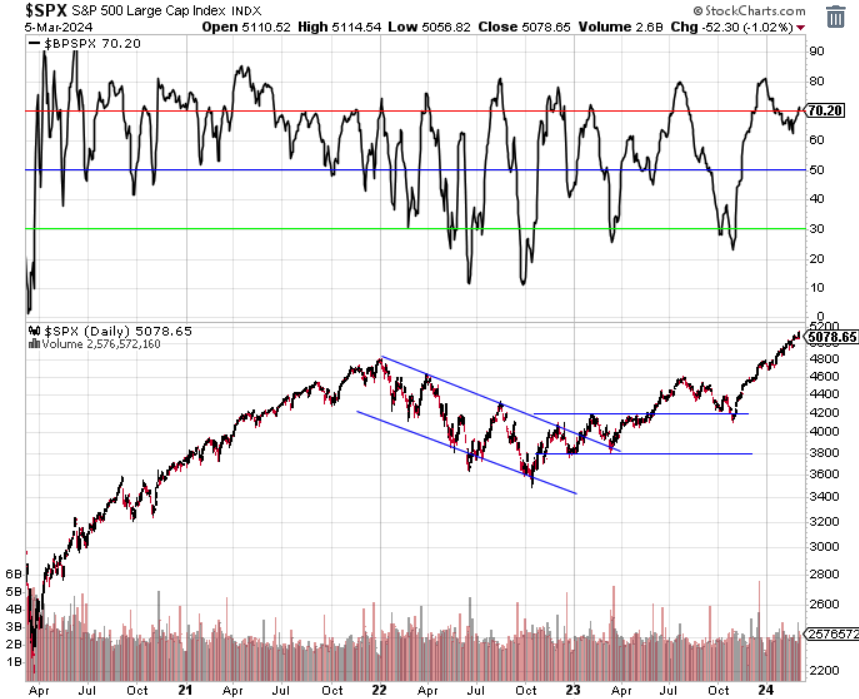

While this recent stock market thrust has been impressive, it may be due for a breather. Our participation model is showing that there could be some additional longevity to this move. Although market behemoth Apple is down 15% from all-time highs while the stock market is hitting new all-time highs, broader participation in the stock market is much better so far this year than 2024. Said another way, more stocks are leading this move higher, even without the help of some tech giants.

Sentiment cooled a bit, but earnings from artificial intelligence leaders like Nvidia and Super Micro Computer didn’t allow for even a brief reprieve back to the middle blue line. Again, sustainability becomes an issue for this current rally given how far stocks have come in such a short period of time. We’d like to see a mild pullback, but we have seen recent years like 2017 and 2019 where stocks just plowed higher all year long.

Interest rate policy remained at 5.25-5.5%. What’s interesting now in the interest rate market is that the combination of the Federal Reserve’s willingness to keep rates higher while risk assets rally higher (in anticipation of rates cuts, of course) is that the interest market has adjusted its expectations from a 1.5% point reduction in 2024 to 0.75% point reduction in just two months. The Fed, for now, seems intent to get inflation back to their 2% target before cutting rates, although recently Fed Chair Powell walked back the “need” to get inflation back to 2%. Until the stock market or economy cools, the Fed has little incentive to cut.

Global Equity: Going Strong

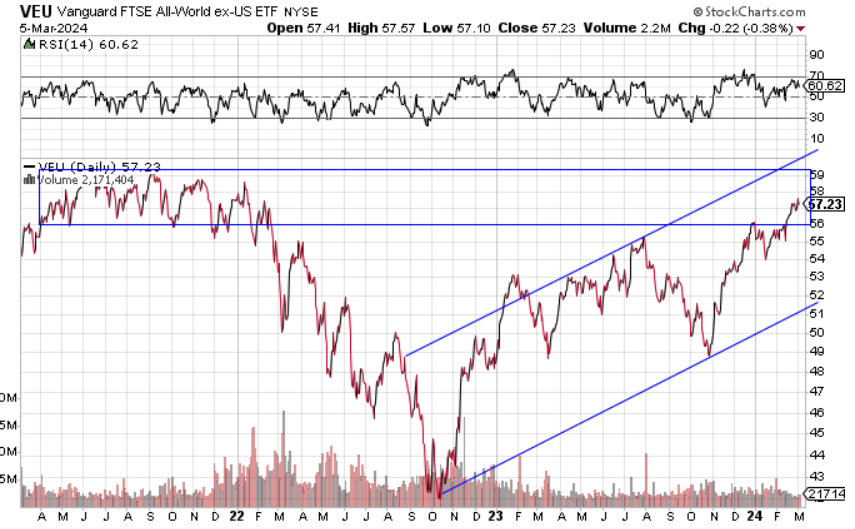

Global equities went higher in the month of February. The global stock market continues to run higher holding a relatively wide upward moving channel. We are now running into a lot of prior selling interest from highs in 2021. Although we are seeing blue skies for the global economy in the back half of 2024, global equities may spend some time consolidating at the prices until then.

China is approaching the 2022 lows as it remains in an economic downward spiral. As the chart below shows, China has been in a distinct down trend for over three years. There seems to be no amount of stimulus their government can throw at their markets or economy to boost stocks. This will be worth watching as China is still a key economic driver in the global economy. Additionally, when sentiment is this low, reversals (higher) could be just around the corner.

Real Estate: Support Where It Was Needed

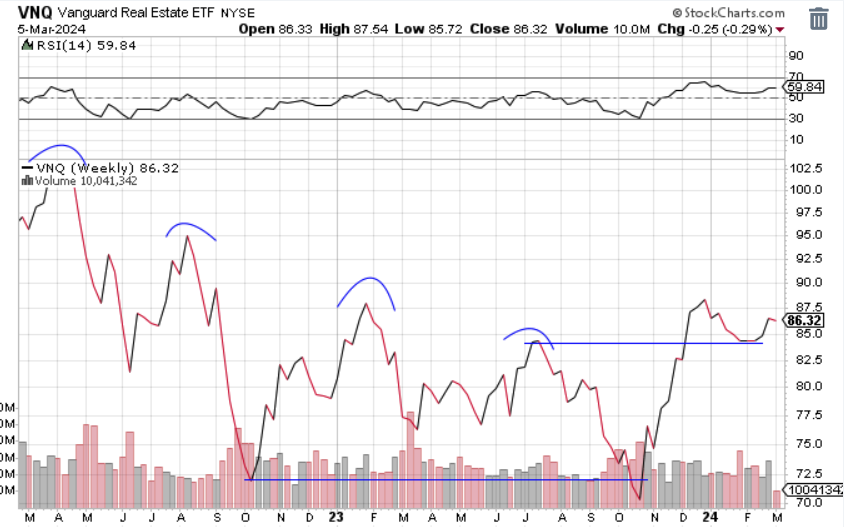

The broader economy continues to perform better than expected, leaving little to complain about aside from some sticky inflation. However, the one fly in the economic ointment is commercial real estate. We continue to see issues in this space as large, vacant office and retail buildings have lost significant market value, causing owners to walk away rather than refinance. That backdrop made the most recent stick save by the real estate market (see below) all the more impressive. We are invested in this sector as directed by our model, but have entered cautiously, as there are underlying problems here that haven’t surfaced yet.

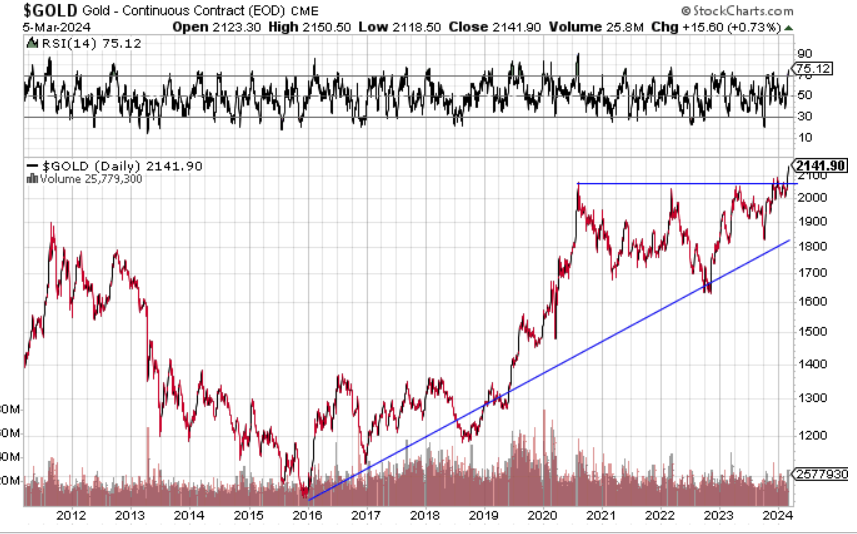

Commodities: Gold Takes Flight

Commodities as a broad basket continue to stay stagnant. Gold, however, just took off to a new all time high – an impressive move as it was not aided by a pullback in interest rates. The breakthrough area around $2050/oz for gold was a point that was tested four different times over the last four years, so this break through and subsequent follow through should end up holding any retest and setting the stage for a significant run higher. Additionally, this breakout was accompanied by big volume, something the last (temporary) breakthrough lacked. This has the makings of a very bullish long term set up.

Fixed Income: Is This Time Different?

Bond yields were up again in February, putting bond prices in the red to start the year. The key 4.25% level on the 10-year U.S. Treasury bill held for now. If yields continue to linger around the green line, this may be an indication rates are interested in heading higher. A move through 4.25% likely puts pressure on risk assets across the board, similar to last year’s late summer move.

The yield curve continues to remain inverted, meaning long term rates are lower than short term. These types of conditions always precede a recession. But with GDP looking positive to start the year, the yield curve inversion is starting to get long in the tooth. In fact, the longest prior inversion was 22 months long and started in 2006, preceding the Great Financial Crisis. Currently we are in month 19 of an inversion. The Federal Reserve is not projected to cut interest rates until July this year, so it seems likely this current inversion will set the record for longest inversion. While this indicator will likely be relevant in the future, the amount of policy levers that were pulled in the last few years may have broken this trust indicator in this economic cycle.

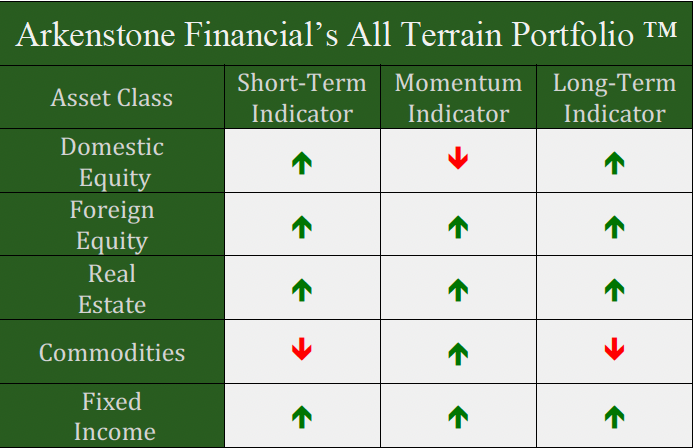

All Terrain Portfolio Update

Our model and indicators had us adding incremental risk into March. We still carry about 30% in risk-averse, short-term treasuries less than three years in maturity that are paying interest in the 5-5.45% range. We will be looking for pullbacks to add risk over the next couple of months to reach full investment as the current risk/reward for risk assets is low. The economic data and outlook remain difficult to forecast but appear moderate to strong as we move into 2024. We will follow our indicators as we wait for investment opportunities, but remain agile within our process as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply