In a Nutshell: On the back of an improving global economic outlook, stocks and interest rates rose across the globe. Risk assets appear to be losing steam internally, as the indices march higher. The Federal Reserve will keep interest rates higher for longer.

Domestic Equity: Indices Make New Highs

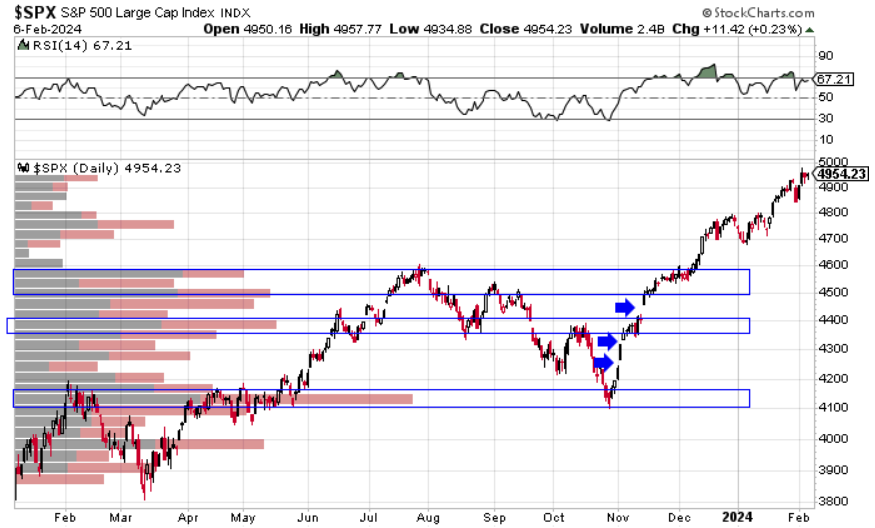

After stumbling out of the gate to start the year, U.S. stock indices finished on a high note. The U.S. economy and corporate earnings remain a bit of a mess, but the net result is that stock indices moved high, albeit with limited participation. U.S. GDP remains stronger than expected (3.3% in Q4, 2023), as was the theme last year. Deficit spending continues, with a significant expansion in government employment. Meanwhile on the corporate side, smaller companies are getting crushed while the behemoths (Amazon and Microsoft, among others) stay strong. Small cap companies are severely negative in growth over the last year, and that can be seen in the price of the small cap index, Russell 2000, which is still down over 20% from its 2021 highs. On the opposite end of the spectrum, earnings so far this quarter have been positive for large companies (the S&P500) and that largely has to do with the top four companies in the index being nearly 80% of the index’s earnings. The net result of all of that juxtaposition is good economic growth, but weak growth when compared to the spending associated with it, as well as good stock market index returns buoyed by a few very strong large companies and limited participation otherwise. The results could certainly be worse, but the sustainability of both the economy and the large stock market indices comes into question. Seasonal weakness tends to arrive for stocks as the calendar flips to February, so we’ll keep an eye on out for pullbacks to add risk into.

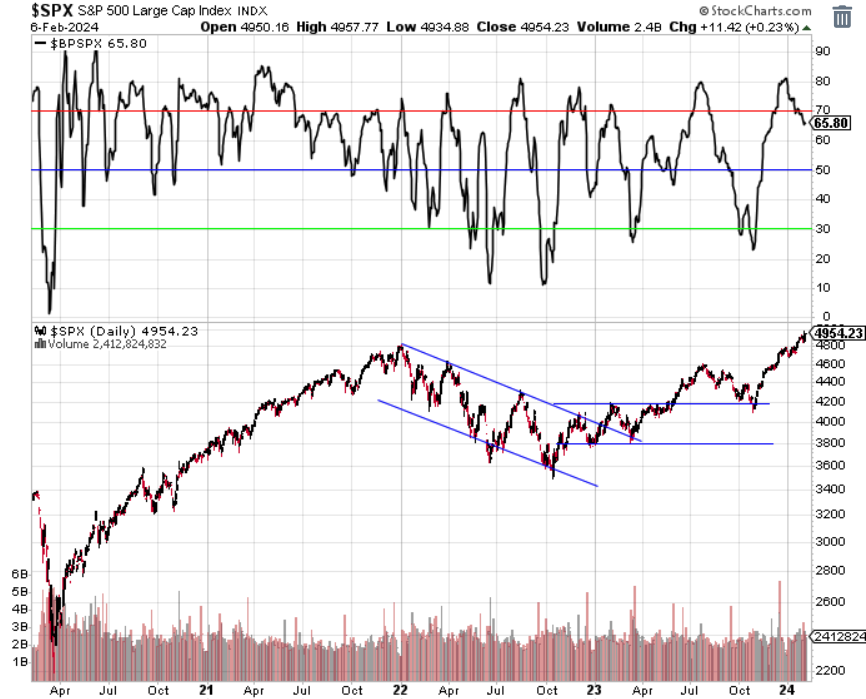

Below, our participation model shows what was described above – a rising stock market with participation falling. This has been a shared characteristic of all local market tops over the past three years.

Sentiment is cooling off as stocks rise as well, indicating market participants are hesitant to buy at current price levels.

Another short-term concern is that the stock market has been anticipating interest rate cuts in 2024, but did not get one in January and is unlikely to get one in March. Federal Reserve Chairman Powell held interest rates firm this past month, and surprisingly indicated rates would not be cut in March, an odd and unnecessary comment from the policy maker. As a result, the market has adjusted its expectations from a 1.5% point reduction in 2024 to 1.25% point reduction. The Fed, for now, seems intent to get inflation back to their 2% target before cutting rates. Until the stock market or economy cools, the Fed has little incentive to cut.

Global Equity: China Imploding

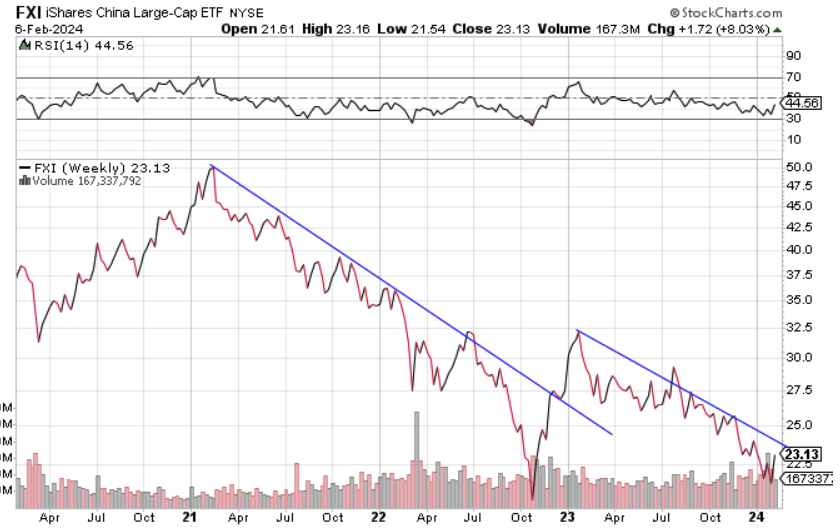

Global equities followed U.S. markets higher to start the year, but were weaker on a relative basis. This was a fairly impressive move for the index, given China’s economic struggles.

China is approaching the 2022 lows as it remains in an economic downward spiral. As the chart below shows, China has been in a distinct down trend for over three years. There seems to be no amount of stimulus their government can throw at their markets or economy to boost stocks. This will be worth watching as China is still a key economic driver in the global economy. Additionally, when sentiment is this low, reversals (higher) could be just around the corner.

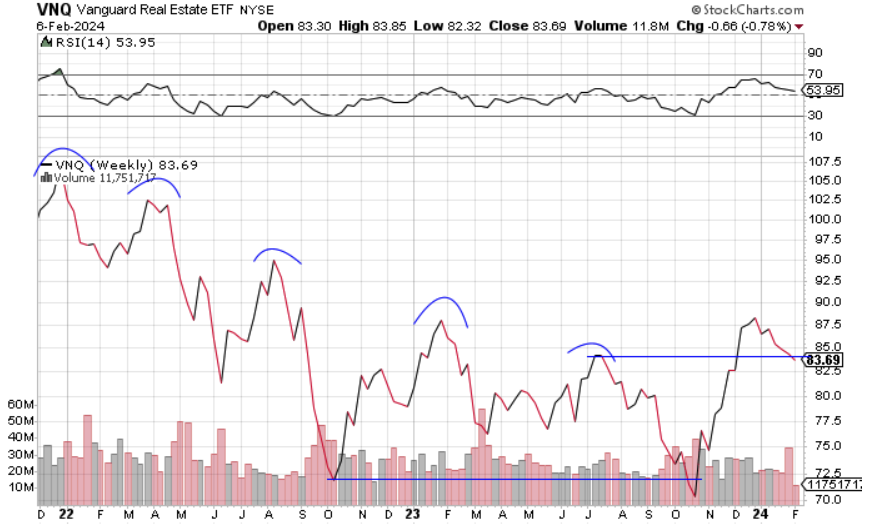

Real Estate: Interest Rate Pressure Is Back

Real estate pulled back over the past month as interest rates picked back up, putting pressure on this sector. The pull back for the sector is back to a spot where we’d hope to see some support and strength. Holding the mid-year peak from last year would set up another run higher. Interest rates continue to dominate this space, so we’ll keep a close eye on this position.

Commodities: Trending Lower

Commodities remain stuck, but on the wrong side of an important level (blue line below). Commodities traded lower to start the year as inflation and global oil demand cooled. From a price perspective, commodities continue to perform quite poorly, displaying textbook downtrend behavior.

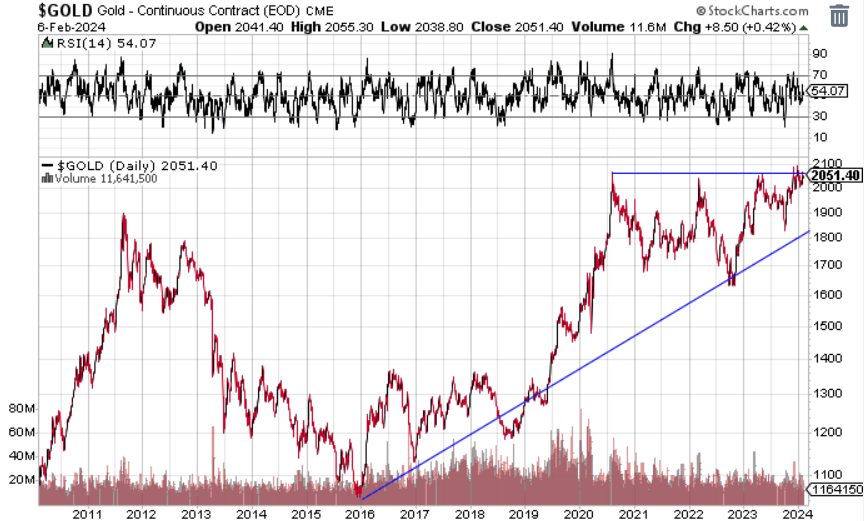

Gold was flat on the month, but in the face of rising interest rates. The two tend to move inversely, so seeing gold hold up with rates rising shows high demand and strength for the yellow metal. The early part of the year typically is strong for precious metals, so we’ll see if that seasonal strength can boost this asset to new all-time highs.

Fixed Income: Rates Are Still the Key

Longer-term interest rates rose to start the year, putting pressure on most risk assets aside from technology stocks. The 10-year U.S. treasury yield is back into the range it traded most of the past year and a half. With economic growth that came in better than expected for Q4, 2023, and initial measures showing more strength into what was supposed to be a weak Q1, 2024 bond yields have ticked higher. With inflation seemingly stabilized and slowing, albeit at higher levels than normal for the past 25 years, yields seem to be moving based on economy growth and how long the short-term rates will be held restrictive by the Fed. Yields at or above the green line likely means no rate cuts from the Fed and good economic growth. Lower down to the red line and rate cuts are coming and growth is slowing.

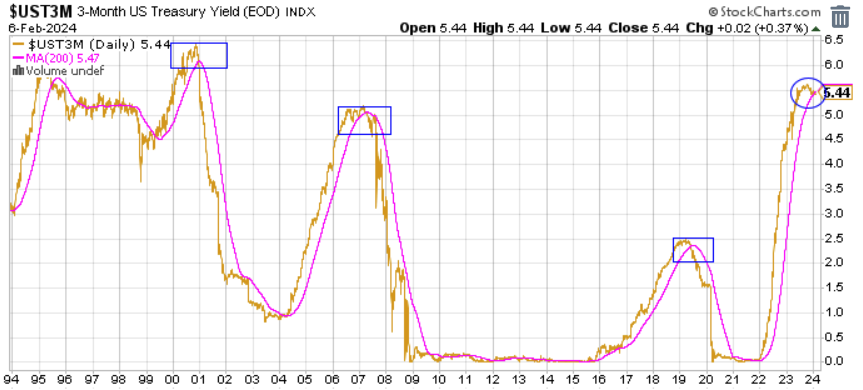

Short-term rates have officially rolled over, as has been the theme prior to most recessions – although we do have a pretty powerful exception in the mid-1990s. This will be an interesting chart to follow because it implies the market expects rate cuts from the Fed. However, what looked to be a weak first half of U.S. GDP to start the year, now looks like moderate to good growth, at least initially. If growth remains strong, the Fed has little incentive to cut rates, yet the market has already priced them in. Something has to give, and the implications will be big for both stock and bond markets.

All Terrain Portfolio Update

Our model and indicators had us mostly steady into February. We still carry about 40% in risk-averse, short-term treasuries less than three years in maturity that are paying interest in the 5-5.45% range. We will be looking for pullbacks to add risk over the next couple of months to reach full investment as the current risk/reward for risk assets is low. The economic data and outlook remain difficult to forecast but appear moderate to strong as we move into 2024. We will follow our indicators as we wait for investment opportunities, but remain agile within our process as new data is presented.

Chart as of 11/30/23

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply