In a Nutshell: Stocks bounced back in October, while rising interest rates continue to put pressure on both the stock and bond markets.

Domestic Equity: Still Looks Like a Bear

Stocks had one of the best Octobers in recent memory, but even that big push was only enough to put socks back into the middle of the down trend. As shown below, it looks like a key level at 3900 has blocked the path higher.

A check-in on our stock market strength indicator below shows we are in what would be the fifth attempt to go positive in 2022. All such attempts failed to break through into positive territory for any kind of meaningful time, marking local market tops. Until we see any sustained time in positive territory, this translates to a bear market for stocks.

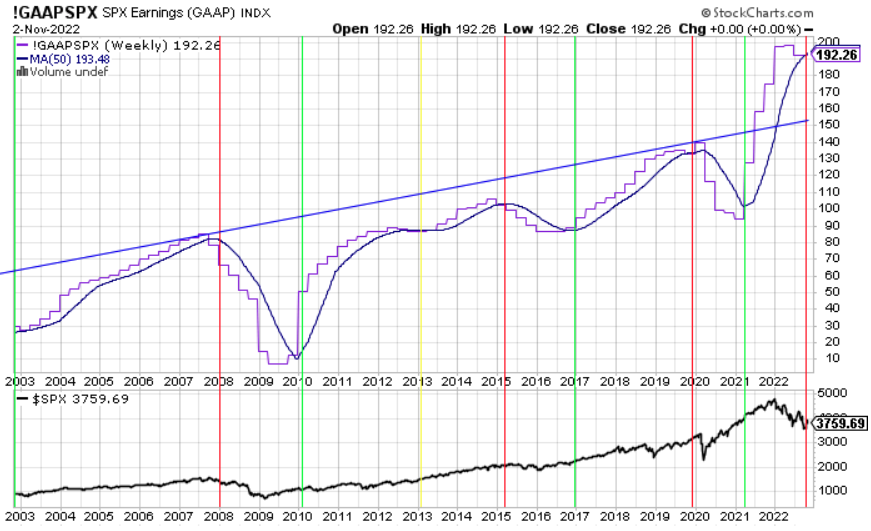

Back in May, we mentioned how bloated corporate profit got during 2021 and that when those profits did cool it would mean another economic headwind in 2022 and into 2023. Revisiting that chart, we are now seeing profits have peaked and are falling (purple) and have just crossed a key indicator (dark blue) that coincides with corporate profit recessions. You can see the prior stock market peaks all coincide with profit peaks and crossing through the blue line is generally confirmation that profits will fall further, along with stocks. We’d expect profits to at least revert back to the blue trend line, but possibly further. Given the poor forward-looking economic and profit data we see, U.S. stocks could stay in a down trend for some time. We’ll avoid the U.S. equities for now.

The Federal Reserve raised interest rates by another 0.75% in the opening days of November. Fed president Jay Powell doubled down on the Fed’s resolute stance in fighting inflation. He reiterated interest rates will be higher for longer than we are used to seeing. He stated that the risk is greater for the Fed to stop raising rates early than it is for the Fed to raise rates so high that it tips the economy into recession. Although many investors have hopes of the so-called “Fed Pivot” to a more accommodative policy stance, the Fed has been very clear that they have no intention of doing so now or in the near future. The bond market expects a few more rate increases from the Fed in the coming months, but likely in smaller increments, with a target of 5%. Of course, this interest rate path is very dynamic, so we’ll continue to monitor closely as it is so impactful for nearly all markets at this time.

Global Equity: Still in Trouble

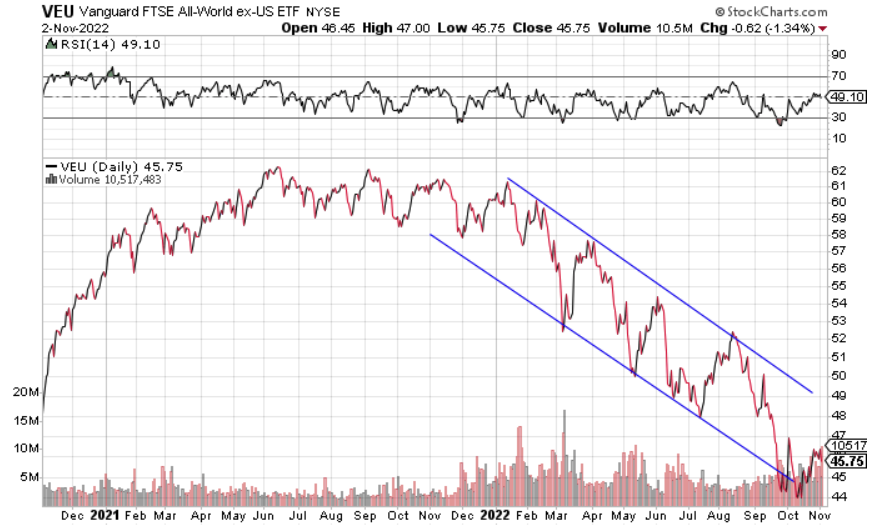

Global markets bounced from new 2022 lows in October. Positives have been hard to come by in foreign stocks in the last year, so this minor bounce is worth mentioning. However, this sector is still in a downtrend. With China still struggling with reopening its economy due to its zero-Covid policy, and Europe battling rising, crippling inflation, a good portion of the economic drivers of the world outside of the U.S. are unlikely to support the global economy in the near future. We continue to avoid this sector completely.

Real Estate: Still in a Downtrend

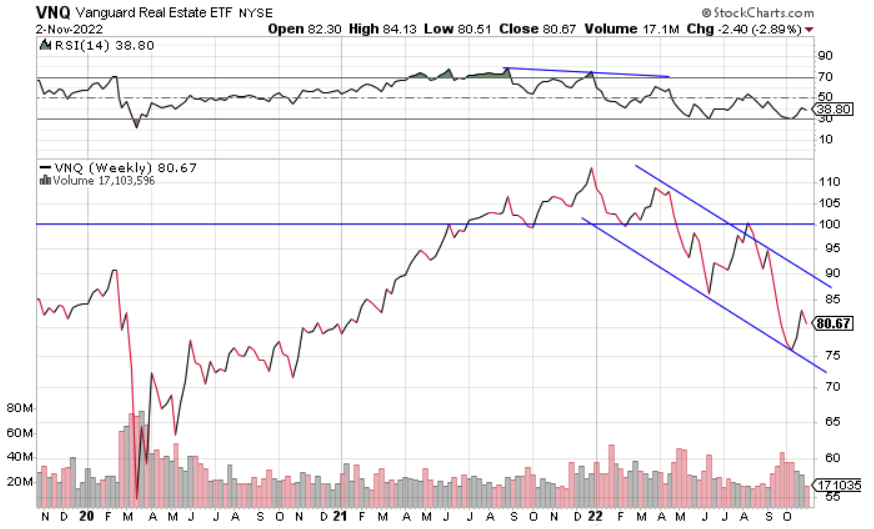

Real estate bounced higher last month, but that bounce still left this sector firmly in a downtrend. With real estate prices still relatively high, either prices or interest rates need to go lower. With interest rates continuing to run higher, it appears prices will continue to suffer for the foreseeable future. We will continue to avoid this sector.

Commodities: Hanging On By a Thread

Like equities, commodities bounced in October – but the bounce was significantly weaker. The commodities complex remains in a similar position to last month as most major trend lines have been broken, but support (the bottom of the blue box) continues to hold. Falling below the blue box would be the last straw for the commodities bull market.

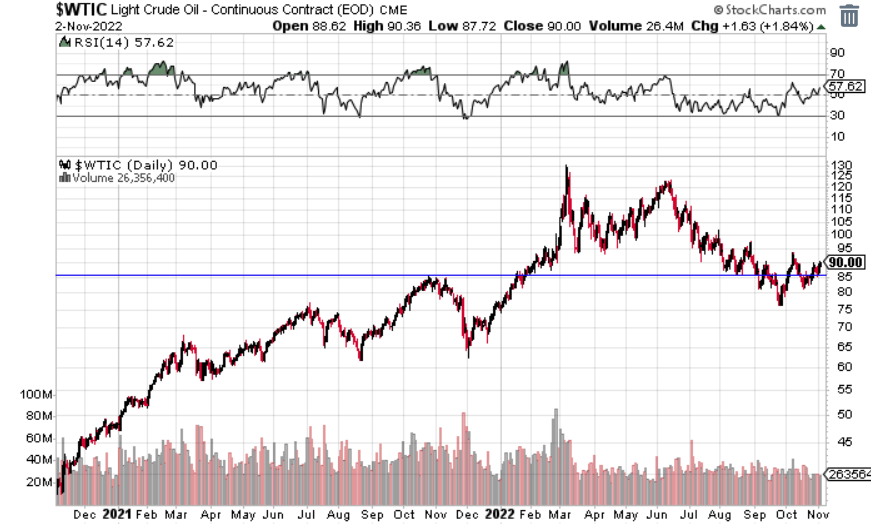

Oil may be the glimmer of hope for the commodities basket to resume its bull market. Oil is now trading above the key blue support line below. The United States has been releasing reserve oil into the economy for the last six months now, suppressing the price of oil. This oil reserve release program is set to expire after the November U.S. elections, so oil may be building strength into that event, looking to run higher.

Fixed Income: Rates Continue Higher

Interest rates continue to trend higher, pushing bond prices lower. You can see from the chart below the 10-year U.S. Treasury is now comfortably broken through the four-decade-long interest rate downtrend. Interest rates are now at levels we last saw fifteen years ago.

Interest rates on shorter time periods are rising much faster than those further out in time. We’ve already highlighted how the 10-year versus two-year yield has inverted (a recession warning indicator) but now the 10-year versus three-month yield has inverted as well. By the Federal Reserve’s own admittance, they prefer the 10-year/three-month yield curve to measure rising risk. Their latest rate hike pushed this inversion into existence. You can see below, the 10-year versus three-month yield inversion signal has preceded our most recent recessions. What’s interesting this time around is that the stock market is already down significantly before this particular inversion occurred. So it’s possible there is more downside ahead for stocks.

Given the unique backdrop in the bond market, there are very few options to choose from that don’t depreciate in value in this environment. We’ve been able to hide out in short duration bond positions to collect (rising) interest while avoiding the loss of bond value. We’ll likely have to stay in these positions until the Federal Reserve stops raising rates.

All Terrain Portfolio Update

Our signals and indicators dictated that we remove the final small remaining risk assets. We hold 100% cash and short term notes in the All Terrain Portfolio. We will continue to exclusively hold safe positions that pay interest until the investment backdrop improves for risk assets. Despite the wide ranging potential investment exposures allowed by our model, there are very few investment options that currently fit our criteria. We will continue to wait for investment opportunities, and in the meantime, follow our indicators and process to adjust risk as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply