In a Nutshell: Volatility continues to rise in equity markets across the globe as stocks sell off. Commodities and oil soar as interest rates begin to retreat.

Domestic Equity: The Downtrend Persists

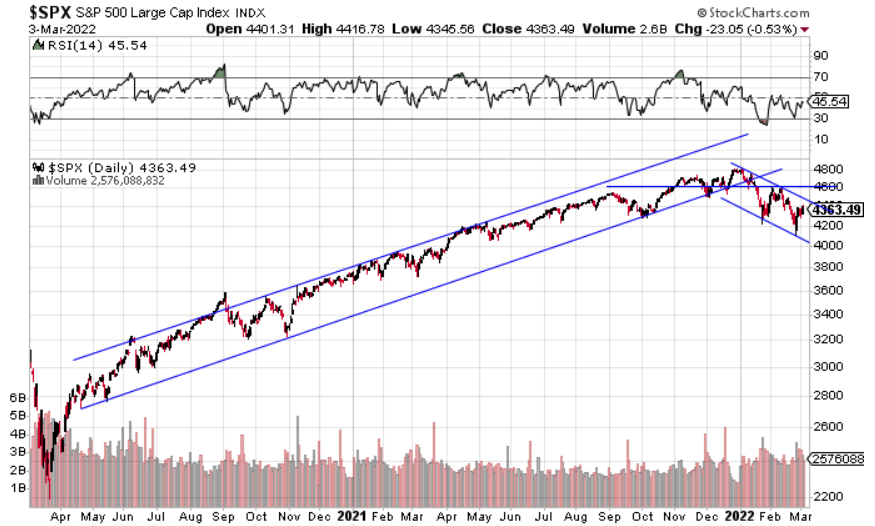

U.S. equity markets closed lower in February, making it two straight down months to start 2022. The Ukrainian conflict has grabbed most of the headlines over the past month, but it is the potential fallout of the conflict that has risk assets selling off. Said another way, this conflict may be the catalyst, rather than the cause, of a deeper stock sell off. The U.S. economic backdrop will be entering a period of slowing during the first half of this year while inflation is high. The Ukrainian conflict occurs in a region that is a heavy exporter of energy and food commodities. Restricted access to those commodities from the conflict has pushed prices much higher, likely pushing inflation higher. The Federal Reserve has said it will combat inflation with higher rates. Stocks are selling off in response to the potential that this catalyst has exacerbated either higher inflation or higher interest rates, or both – thus putting additional pressure on an already slowing economy. Below, you can see textbook bear market behavior in the S&P 500 and the Nasdaq. These downtrends are being clearly defined by high volatility and vicious upside rallies that can’t take out previously made local high values.

There is an old saying in the investment world that goes something like, “there’s always a bull market somewhere.” Luckily for us, we are able to participate in a few currently – one of them being the energy sector of the stock market. Energy prices have been trending higher for over a year, so the companies that produce and sell these commodities have been able to maintain a strong uptrend, as shown below.

All eyes will be on the Federal Reserve at their upcoming meeting this March. This is when the widely anticipated first rate hike is projected to happen. The context they provide with the rate increase will be important for markets. The Fed is now faced with the nearly impossible task of fighting inflation without prohibiting economic growth.

Global Equity: Nosedive

We’ve documented how the broad global equity markets have been unattractive investments for over a year now. The bearish trends that have been in place for months at both the developed and emerging market level have now accelerated to the downside, breaking below the already downward sloping trend channel. In other words, these markets have gone from bad to worse.

The main drivers of this move lower are the Russian and Chinese stock markets, which have had outside impacts on these broader markets because of the depth of their crashes and the size of their impact. The Russian and Chinese stock markets are down roughly 80% and 40% respectively. Outside of some specific countries that are faring okay, there is no reason to have global equity exposure.

Real Estate: Could Have Been Worse

Real Estate continued lower in February, but when compared to the stock market, it held up relatively well. The big reason for that was the rapid pullback in interest rates. Real estate is interest rate sensitive, and when rates fall, that’s a boost to asset pricing. The chart below looks a lot like the equity charts we highlighted above, with the clearly defined pattern of lower local high values. If interest rates continue to fall, real estate could be a place for investors to profit even in a bear market for stocks. We’ll need to see the index shake its bearish price patterns first before we regain interest.

Commodities: Commodities Go Parabolic, Gold Breaks Out (Finally)

As mentioned in our U.S. Equity section above, the Ukrainian conflict has sent many food and energy prices soaring. The chart below highlights that move with a parabolic move higher. Parabolic moves are not normal and typically unsustainable in the long run, but can run much higher in the short term. When these types of moves stop, they tend to reverse quickly, making it a high risk, high reward investment. Any sort of quick peaceful resolution to the Ukrainian conflict could bring energy prices and food back down quickly. The flipside of that is the longer this conflict remains, the higher these prices will have to go. As long as this conflict continues, energy needs will likely increase and crop yields will likely fall, putting upward pressure on prices.

Gold finally broke through its consolidation range to the upside as we’ve been suspecting for the past few months. This price action is a good reminder that gold is much more sensitive to interest rates than the widely perceived inflation rate. Rates went higher last year with inflation, while gold went nowhere last year. Interest rates have finally turned down and gold subsequently has gone higher. The broader backdrop of falling global growth and military conflict and sanctions that are weakening currencies across the globe will likely be tailwinds, as long as interest rates continue lower.

Fixed Income: Are Rates Done Going Up?

Last month we highlighted how the bond market was sending mixed messages. That message is still mixed, but perhaps starting to become more clear. Interest rates took a massive dive lower on the 10-year U.S. treasury note. The 15% move lower over just two trading days ranks as one of the biggest moves we’ve seen in the last few decades. The question is what drove this capitulation. This could be a big reactionary move as investors move out of risk assets and seek safety. This also could be the bond market starting to look through inflation concerns of the present and focusing on potential economic slowing of the future. Either way the price action will be key. The 1.7% level has held for now, but if it’s broken, it would mean the bond market has flipped bearish on the U.S. economy.

We see a similar move on the 30-year U.S. treasury note below, on a much larger scale. The 30-year interest rate seems to have reversed at the 2.3% level which is a logical long term pivot based on the chart below.

Longer term interest rate moves after the Federal Reserve starts raising short term rates will be critical in helping understand the future outlook for the U.S. economy.

All Terrain Portfolio Update

Our indicators and models had us only make small tweaks to our already very defensive positioning in the All Terrain Portfolio. Our positioning has allowed us to produce modest gains in the face of stocks selling off this past month. We will continue to follow our indicators and process to adjust risk as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply