In a Nutshell: Interest rates continue to rise, pushing bond prices lower while stocks fall in the U.S. and across the globe.

Domestic Equity: Risk Appetite Has Shifted

Last month we posited the question of what was driving the increase in volatility to close out the year. Was it just normal rotation and investor repositioning, or was selling distribution afoot? We received a very loud confirmation of the latter in the month of January. At the lowest point of the month, the Nasdaq Index was down nearly 17% from the November peak, the Small Cap index – the Russell 2000 – was down 20% and broader indices like the S&P 500 and the Dow Jones Index were down 10%. The charts tell the story as clearly defined trends were broken to the downside on rising volume in the Nasdaq and the Russell 2000.

There are some pockets of strength if you drill down, but they are mostly in the defensive portion of the stock market like utilities and consumer staples shown below.

Since the March 2020 bottom, any kind of stock market weakness was bought by investors. There was always some combination of government stimulus and economic recovery that made buying the dip a risk worth taking. However, we are entering a regime change in both the government’s policy support and economic data. There is no economic stimulus on the government docket as of now. Our economic data looks to be cooling and likely will continue to do so through the first half of the year. On top of that, inflation continues to stay higher than expected so interest rates are set to rise, putting additional pressure on the economy. Said another way, our economy will be slowing while financial conditions are tightening, or less supportive of growth. This type of backdrop has traditionally been challenging for risk assets like stocks.

Speaking of inflation and rising interest rates, the Federal Reserve has clearly signposted that they intend to raise rates to combat inflation. The bond market is now pricing that the Fed will raise rates at a 100% certainty at their next chance to do so in March. Currently the bond market expects between five and six hikes by year end. The Fed has found themselves in a tricky situation where they must either choose to raise rates to combat inflation and risk slowing the economy down further, or leave rates low to support a slowing economy, potentially allowing inflation to rise even further.

Global Equity: Relatively Better, Still Red|

Global stocks sold off to start the year, but fared better than U.S. stocks in January. This relative strength is good to see, but when we dig into the trends, as you can see below, they are negative in both the developed and emerging markets.

Outside of some specific countries that are faring ok, global stocks will likely be dragged down by any domestic stock weakness for the foreseeable future.

Real Estate: The Uptrend Finally Breaks

Last month we talked about how real estate has been taken to the brink, but held its trend, just barely. The start of 2022 brought a clean trend break in the real estate sector. The sector is now clinging to price support from last year that must hold if prices are to go higher. Real estate is interest rate sensitive, so when rates rip higher like they did to start the year, prices fall as affordability falls. With the Fed almost certainly to raise rates, the sector may have a tough start to the year. We’ve reduced our exposure and will continue to monitor.

Commodities: A Huge Reversal?

Last month we highlighted what appeared to be a trend breakdown in the broad commodities space. We update that view to show that commodities are attempting to get back on trend, making a higher price point for the first time in three months. The commodities space will be a must watch for inflation insight over the next few months as what appeared to be a topping sign has developed into a reacceleration. The interesting part of this move is that it is almost entirely being driven by oil – most other major commodities are not making new high prices along with oil – but it is still enough to push the sector higher as a whole.

Gold continues to narrow its trading range while consolidating. This price action tends to lead to large moves either way as price energy has coiled for nearly a year. We’d give a slight edge to an upside breakout given the current economic backdrop, but it appears patience will be needed for the eventual answer.

Fixed Income: Rising Rates Create Chaos

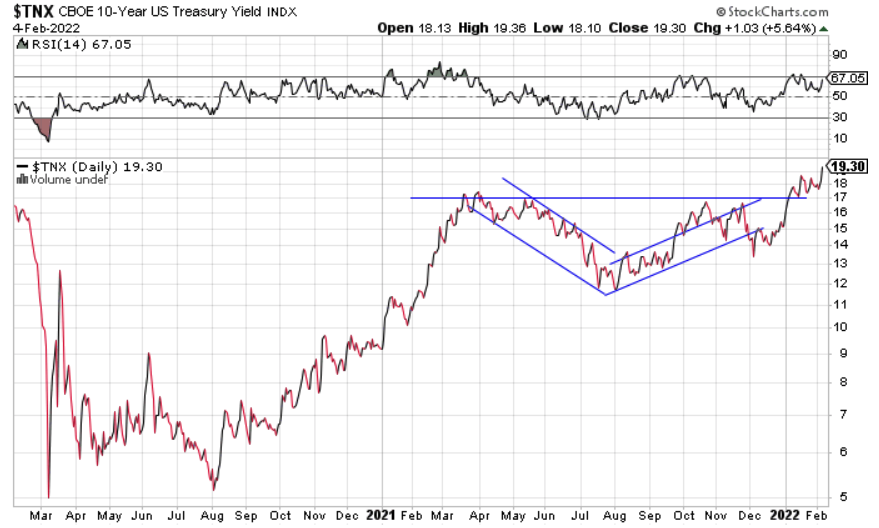

Interest rates broke out in a big way to start the year. The bellwether 10-year U.S. treasury note has now broken out and is trading higher than it has at any point post-Covid.

The two-year note interest rate has risen five fold in less than six months.

Rising rates are typically a good thing, as they tend to foreshadow economic growth the further out you look. However, the further you look out in the U.S. bond market, the less interest rates are rising. Here’s the 30-year note with rates safely below early 2021 highs.

This mixed message from the bond market seems to be telling us that short-term interest rates are going to rise through policy decisions, while the long-term rates are concerned about future economic growth.

What makes our current scenario even more interesting and perhaps challenging is that these rises in interest rates have been occurring while stocks are selling off. For the better part of the last 40 years we have seen interest rates fall – and we’ve grown accustomed to seeing them fall specifically when stocks fall, giving bonds a price boost and a natural portfolio hedge for the traditional stock and bond buy and hold portfolio. Currently, traditional investors are seeing both components – stocks and bonds – fall at the same time. If this short-term relationship continues, there could be big implications for future portfolio construction for long-term investors.

All Terrain Portfolio Update

Our models and indicators had us positioned defensively to enter 2022, and last month’s sell off has our model increasingly defensive with an even higher allocation to cash. We will continue to follow our indicators and process to adjust risk as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply