In a Nutshell: Broadly, risk assets finished 2021 very strong, despite a lot of volatility and noise. Inflation continues to be the primary driver across all assets, but not all markets agree on where inflation is headed next.

Domestic Equity: Rotation, Fear, or Inflation?

What a noisy month December was for the U.S. stock market. You can see from the chart below December had all sorts of drama: it tested the low end of the channel twice and still finished the year at an all-time high. There is much to unpack from this past month, as there is more going on under the surface than the index would indicate.

Let’s start with software, one of the best-performing sectors over the past decade. You can see the six-plus year trend of out-performing the stock market was broken. This seems to be primarily driven by inflation concerns as higher inflation will lead to higher interest rates which make these leveraged companies a little more expensive to maintain, potentially reducing future growth.

Next we see the monster bump in value/dividend stocks against the stock market. These companies are considered to be higher quality than most stocks. This was an interesting shift as the mega-cap tech companies had been keeping the index afloat for so long. It is interesting to see support come from somewhere else, though this is a defensive play by investors. It seems that under the surface, the stock market is worried about inflation going higher.

Much of the stock market concern on inflation was stoked by the Federal Reserve. They have been hammering home at every opportunity that they no longer view inflation as temporary but instead as persistent, and that they will need to raise rates and reduce economic stimulus. This approach, if applied, will effectively be a double economic tightening which would likely put a lot of pressure on the economy. It remains to be seen when and how much they tighten.

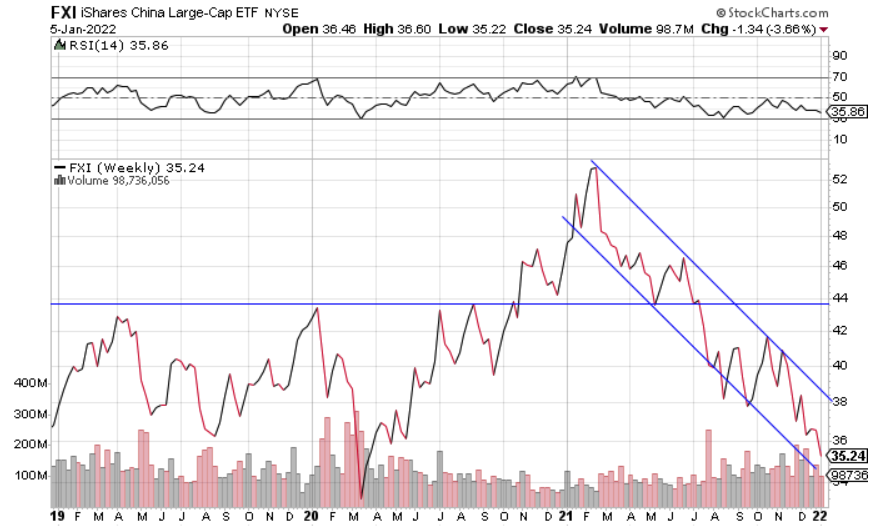

Global Equity: Are We There Yet?

Emerging markets continue to tread in no-man’s-land. This long, methodical march lower ended up yielding a negative return in 2021– one of the few indices to do so last year. There are some signs of life on the price chart below, albeit subtle. We are seeing what could be a higher local low value right now, which could propel price through 50 and out of this downtrend.

If a breakout is to happen, China will be the catalyst. After a terrible 2021, China’s economic data is starting to see signs of life. Any support or growth from China could give the whole EM complex a boost.

Real Estate: Blast Off into Year End

Last month we talked about how real estate has been taken to the brink, but held its trend. That was the recharge needed to close the year out very strong, setting new all-time highs. With 2021 in the rear view now, the focus in 2022 for real estate will be interest rates and, by extension, inflation. Higher inflation from here would drive rates higher as the Fed has already indicated their willingness to raise rates in 2022 to combat inflation. Inflation is high right now and has not fallen yet, but we are seeing shipping bottlenecks subside and input prices fall for producers, an early indication of slowing inflation. A goldilocks scenario for real estate investors would be high (but falling) inflation, reducing the need for the Fed to hike rates. In that scenario, that would likely provide investors with both the boost of higher prices through inflation and low rates.

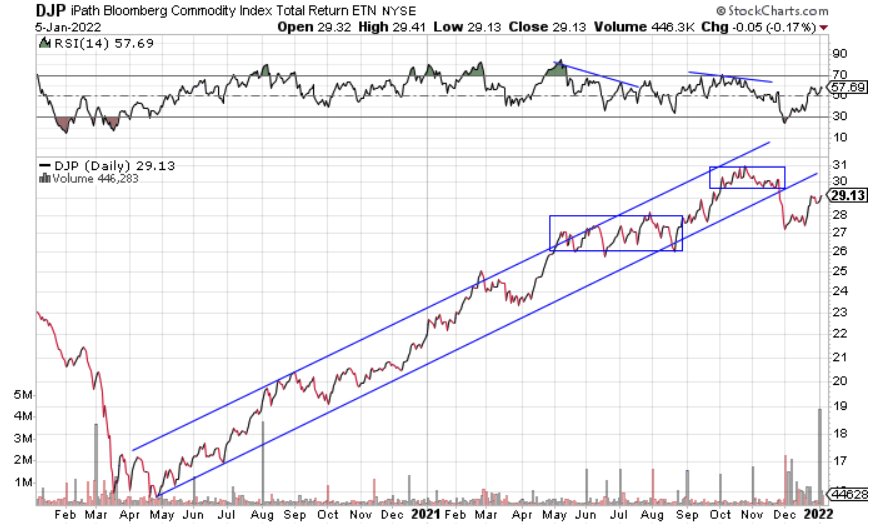

Commodities: Breaking Trend

We hinted at a trend break last month in commodities. While we have seen some price recovery since then, there is still a lot of work to be done to get us back in the raging bull camp. We are still trading below the trendline and most recent higher consolidation (top box). Price will have to trade back in the 30s to get our attention. The context right now is different for commodities as well. As we mentioned in the real estate section, we are now seeing mixed inflationary pressures, versus overwhelmingly strong inflationary pressures throughout 2022. Commodity prices seem to indicate that at least for hard and soft goods, the highest inflation may be behind us.

Checking in on gold once more, we see it is picking up steam within a large consolidation. We will need to see a breakout above the top blue line to confirm the next move higher.

Fixed Income: Make or Break Time for Bonds

The 10-year U.S. treasury bond interest rate is now back up to where it traded about nine months ago. The context is a little different this time around as inflation has risen about 35% since the last time 1.7% on the 10-year was reached.

If we look at the relationship between inflation protected treasuries and regular treasuries below, it’s interesting to see that this relationship is now under the trendline and has been rejected on its most recent attempt to breach it. This suggests that inflation is not as much of a driver of the rise in rates as it was in the second quarter of 2021. This will be very interesting to watch play out. Especially considering the Fed and commodity, stock and bond markets are all not in consensus on inflation going forward.

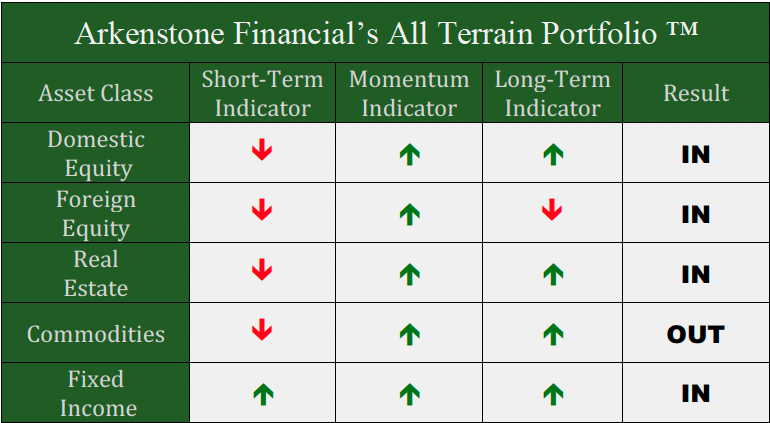

All Terrain Portfolio Update

Our models and indicators have shifted a bit more defensive for the second consecutive month heading into 2022. We will continue to follow our indicators and process to adjust risk as new data is presented.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

- Interest Rates Stabilize, Stocks Bounce - September 6, 2024

Leave a Reply