In a Nutshell: Stock indices across the globe experienced their biggest pullback in nearly a year, while commodities and interest rates continued higher.

Domestic Equity: Stocks Fall, Finally

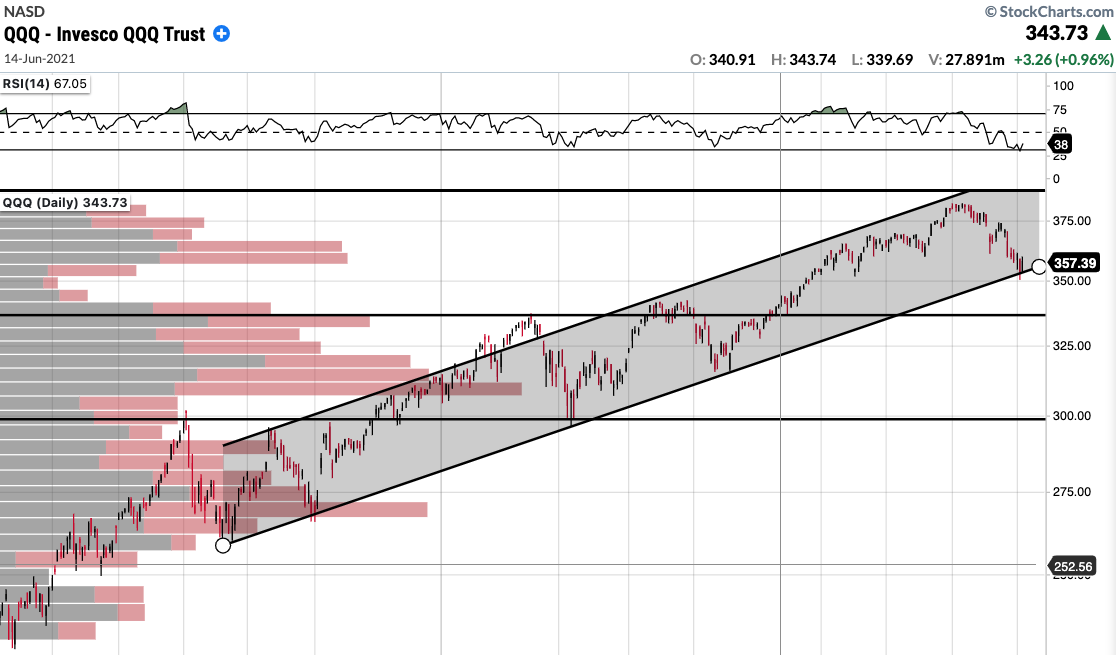

Stocks sold off about 5% in September, capping the weakest month for stocks in a year. September and early October are traditionally the weakest times of the year for U.S. stocks, and this year was no exception. Add on the decaying economic data due to Covid variant scares, and you get a recipe for a modest stock pull back. Although October will likely be choppy and volatile with so many fear-inducing narratives running through headlines, we’ll look for stability mid-month when large companies begin reporting, what looks to be, promising earnings results. Additionally, the Delta variant scares may have pushed more growth into the fourth quarter than initially expected, potentially setting up a strong close to the year. If the chart below of the Nasdaq is an indication, this recent sell off might be a good buying opportunity within an uptrend. You can see the channel below has provided good entry points over the course of the last year.

Not all stocks sold off in September. The oil and gas companies of the energy sector were up 13% in September pushed higher by rising oil prices. The energy sector is still working within a larger consolidation since March, so a breakout here could set the stage for a big run higher.

The Federal Reserve continues to remain accommodating with emergency-level treasury bill purchases, or quantitative easing. The Fed has hinted at a willingness to reduce this economic support in the next month or two if jobs reports and economic data support the decision. The Fed has also indicated that it may raise interest rates near the end of 2022, which is sooner than the previous target of 2023. The Fed is not worried about inflation, but has acknowledged that inflation is higher than expected.

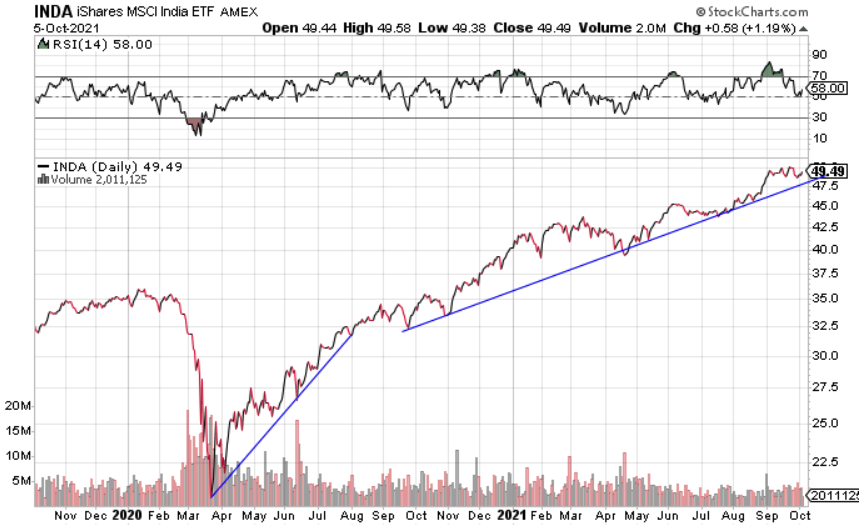

Global Equity: Emerging Markets are Slumping

Checking in on emerging markets (EMs) shows a pretty ugly chart. The broader sector is down about 10% over the course of the last six months. This is largely a result of China’s continued weakness and sheer size bringing down the entire group of countries.

There is one bright spot in EMs, and that’s India. Although the country suffered a Covid scare this past spring, the country has held one of the strongest recoveries of any country across the globe. Coupled with a growing economy and young demographics, this is a country to watch both in the short and long term.

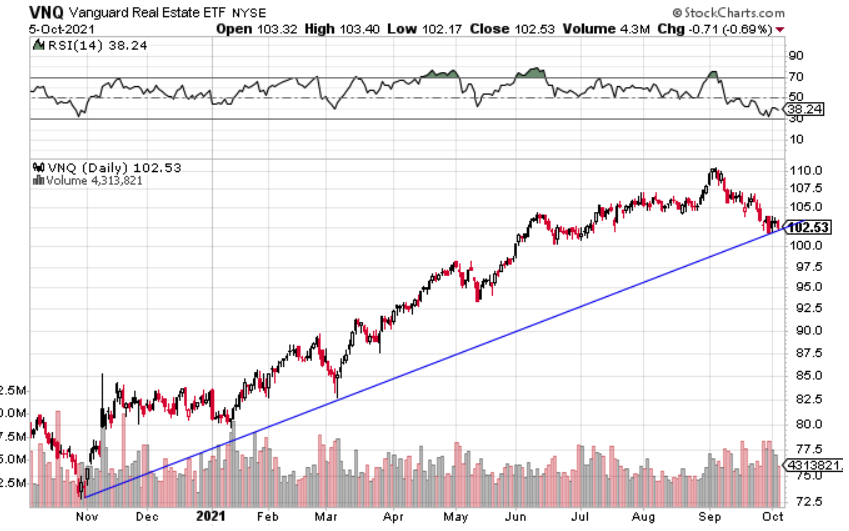

Real Estate: Needs to Hold the Line

Real estate has been one of the strongest performing sectors of the U.S stock market this year, but has hit a rough patch in September. Losing 7% on the month, real estate, was one of the weakest sectors. As you can see below, real estate is at the brink with respect to the nearly year long trendline. With economic data looking to improve into the fourth quarter of this year, and seasonal weakness in the stock market nearly behind us, holding this trendline could be a sign of good things to come as we head into year end.

Commodities: Breaking Out

Last month we showed how commodities have been in a consolidation for months. Although price momentum had been fading for months as well, this consolidation ultimately resolved in the direction of the broader trend: up. Commodities broke out to new 52-week highs and were up 7% for the month – in a month when stocks were red.

Revisiting our “stocks vs. commodities” chart below shows a continuation of commodity dominance. When the chart moves down and to the right, that indicates that commodities are the stronger investment, as far as returns, when compared to stocks. After a nearly decade-long dominance by stocks, could we be in store for a secular shift favoring commodities?

Fixed Income: Rates Finally Break to the Upside

Since the Covid-19 market event in March of last year happened, the bond market has frustrated many investors in real-time, but in retrospect has always been correct, albeit early. Remember, bond yields move based on anticipated economic growth and inflation. You can see below in the months prior to the Covid Crash last March, bond yields fell precipitously, indicating that bond investors saw deteriorating growth on the horizon. History shows this to be the correct call as stocks soon plummeted. After months of following turbulence, yields finally took off again at the end of 2020 and into 2021, with stocks running higher alongside. The bond market sniffed out deteriorating economic growth this summer and fell, taking stocks down with them, mildly. GDP for the third quarter looks like it will disappoint, due to Delta variant concerns, validating the bond market once again. However, we are now seeing yields rise again into our recent stock market sell off, indicating future economic growth could be on the horizon and this recent stock weakness could be a good buying opportunity. If bonds are correct, a stock market rally into year end could be in the cards.

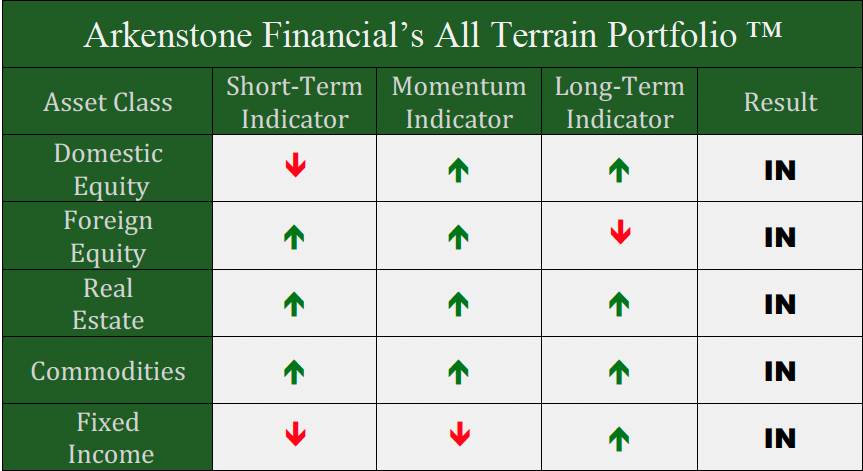

All Terrain Portfolio Update

The All Terrain Portfolio has started rotating out of defensive positions and into more cyclically sensitive and growth oriented sectors on this stock market sell off. We will continue to add risk provided projected future economic data continues to improve. We will continue to follow our methodology and indicators to find buying opportunities and manage risk.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply