In a Nutshell: The U.S. stock market ground higher, but with new leadership as defensive stocks lead the way while economic reopening stocks lagged. Interest rates and commodities remain stuck in neutral.

Domestic Equity: Deterioration or Rotation?

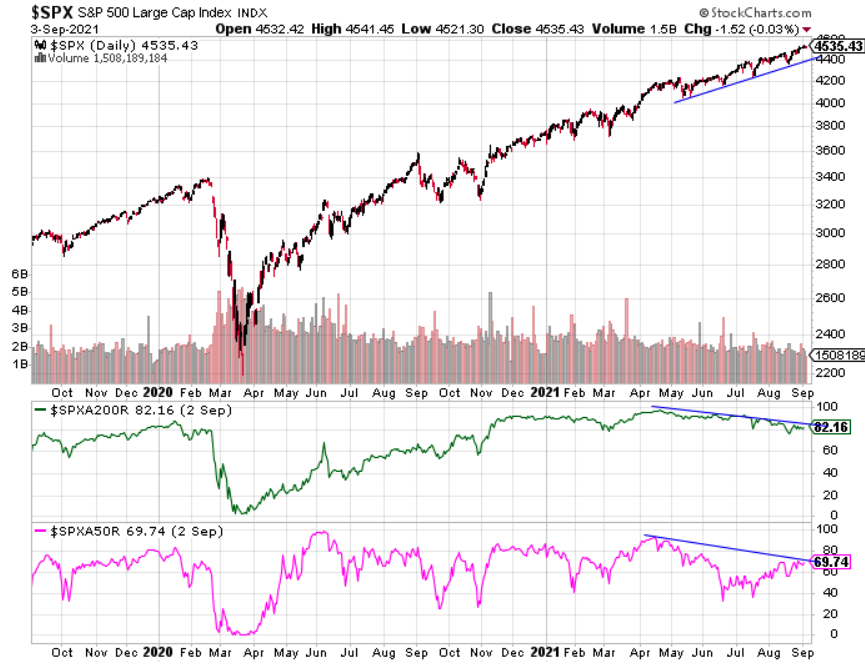

U.S. stocks tacked on another 3%of gains in August. However, the sectors that lead the market this past month were mostly defensive in nature with utilities, health care and technology leading the way. This defensive positioning is likely a result of slowing economic data with investor sentiment softening. This positioning is showing up in market participation as well. You can see below that since May, while the S&P 500 continued higher, the number of stocks trading above their medium and long-term trends (pink and green) have fallen, meaning fewer stocks are participating in uptrends while the indices make new highs. This type of market dynamic can be a sign of market deterioration.

This type of behavior can also be a sign of market rotation. We mentioned previously that if the market rotated out of cyclical positions (like energy and financials) and into more secular trending areas like mega-cap technology, the sheer size of the sector can keep the market afloat. It appears we are seeing rotation, at least for now. You can see the rotation playing out below with a comparison chart of technology against the energy sector. Most of 2020 showed technology leading the market through the Covid-19 collapse of markets. Once the markets were convinced the economy was reopening because of an improving health backdrop last October, the energy sector (as well as the re-opening/cyclically sensitive sectors) led the way until May of this year, where technology took back the reins. This timeline also corresponds with falling market participation in our chart above. The stock market has gone a long time without a significant pullback, so this market price and participation action may lead to deterioration and ultimately a market correction, but for now this is rotation until proven otherwise.

The Federal Reserve continues to remain accommodating with emergency-level treasury bill purchases, or quantitative easing. The Fed has hinted at a willingness to reduce this economic support in the next month or two if jobs reports and economic data support the decision. The Fed has also indicated that it may raise interest rates near the end of 2022, which is sooner than the previous target of 2023. The Fed is not worried about inflation, but has acknowledged that inflation is higher than expected.

Global Equity: Europe, the International Bright Spot

When we turn our gaze outside of the U.S., there is not a better looking price chart than European equities. There is a good reason for that as well. Europe has been one the slowest groups of countries to respond and recover from the pandemic, and thus have more daylight ahead of them. Over the next three to four quarters, Europe is one of the few places in the world where growth is projected to increase quarter over quarter. Europe has underperformed the globe for the last decade, but the table could be set to lead the world, albeit periodically.

Within the Eurozone, the Netherlands have been the brightest star, ripping off 15% in the last two months alone and up nearly 30% on the year.

Real Estate: Recharged and Heading Higher

Real estate continues to stair step up as this sector continues to lead markets higher. After hovering and recharging for the past few months, it continued its textbook technical path higher, breaking out of a very bullish consolidation. One of the sectors driving the non-residential real estate market has been storage companies. With so many home purchases over the last year, storage facilities have been white hot, supporting homeowners during shelter transition. Our data is suggesting a mild slow down in economic growth in the near term is likely, a backdrop that would be supportive of the real estate sector.

Commodities: Boxed In, For Now

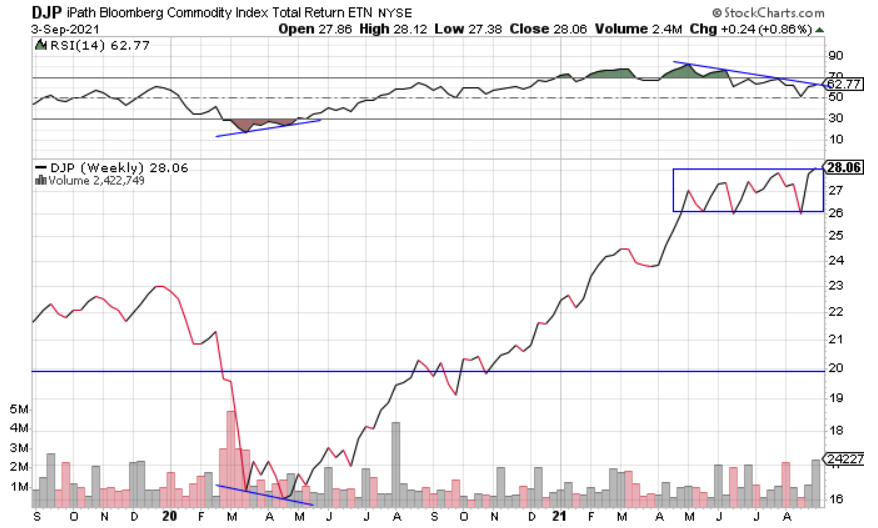

Commodities continue to be stuck around our $27 price target. You can see the box below highlighting the range that commodities continue to be trapped in. Price momentum is falling as well for commodities, which can be a sign that price is mounting a reversal. Although, for now, given the strong long-term uptrend for the sector, the benefit of the doubt should be given to the idea that this is a consolidation within an uptrend. If inflation stays higher for longer, commodities could take the next leg up in price. Commodities appear to be at a fork in the road.

Fixed Income: Inflation Yield

Bond investors continue to face tricky investment conditions. Longer-term yields continue to fall in line with a multi-decade long trend as highlighted below.

However, the key difference right now versus the last 40 years is that inflation is rising and showing signs it may stick around longer than anticipated.

The only place to exploit this rare bond market behavior is in the short-term inflation protected U.S. treasury (TIPs) market. With an inflation adjusted yield of over 3%, short-term TIPs are now paying out a higher yield than investment grade corporate debt. These TIPs have also enjoyed price appreciation while interest rates are increasing (the two trade inversely) due to inflation increases that have more than outpaced interest rate growth. Below, you can see the rare phenomenon where price (black and red) has moved higher in lockstep with interest rates (green). Inflation will continue to be the most important factor for bond investors when choosing their positions.

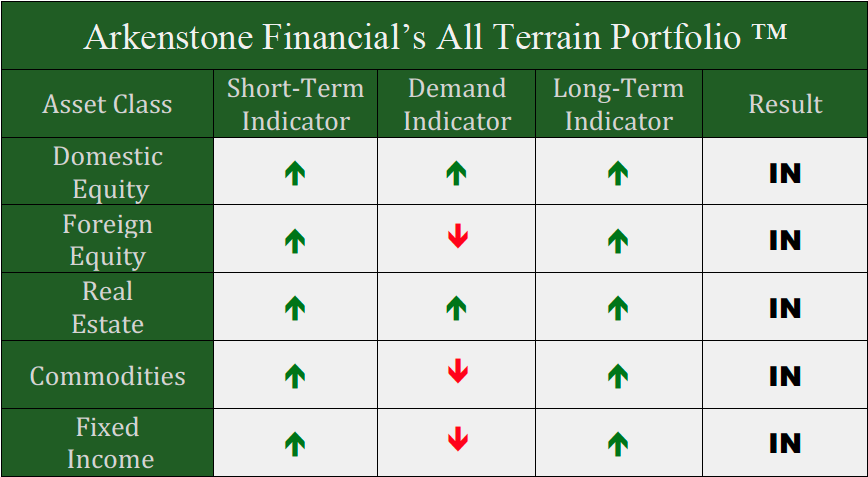

All Terrain Portfolio Update

The All Terrain Portfolio continues to rotate risk into the strongest performing assets within broader sectors. With many economic forces approaching a potential turning point, we have continued taking a more defensive posture. We will continue to follow our methodology and indicators to find buying opportunities and manage risk.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply