In a Nutshell: Global inflation continues to rise, giving a boost to commodities and the related countries and companies. Bond investors find themselves in a tricky spot with rates flat and inflation rising.

Domestic Equity: Stuck in a Range

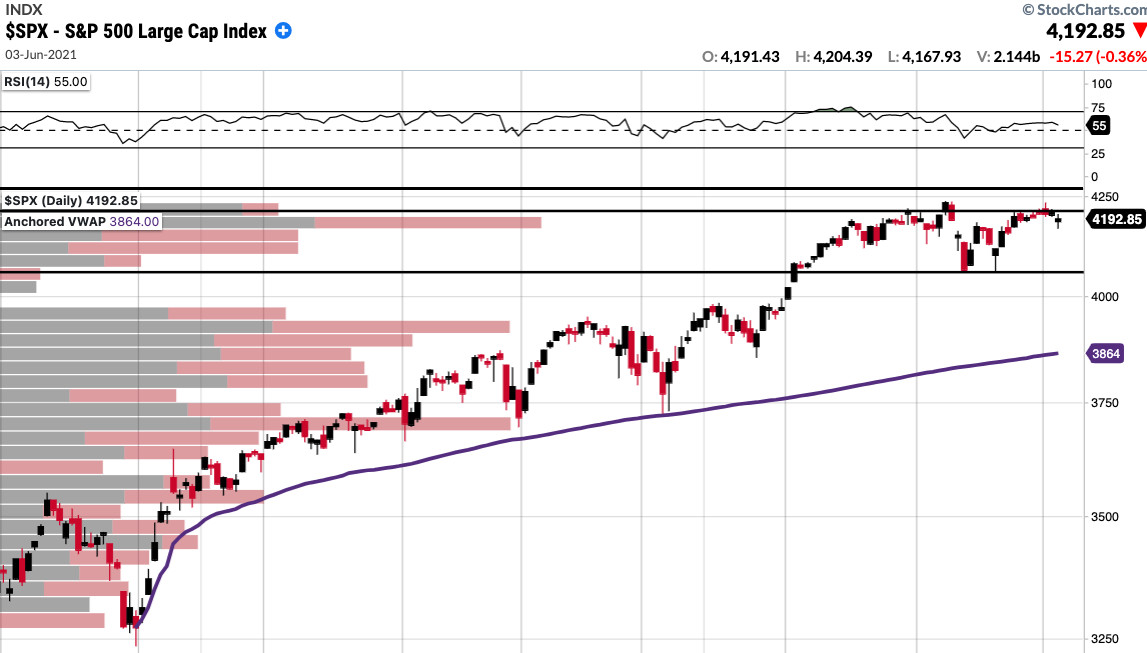

U.S. equities were flat on the month as the S&P 500 index continues to trade in a range for the past couple of months, and is struggling to make new high marks. Ranges and consolidations in an uptrend typically resolve higher, so that seems like the likelier outcome from here. However, you can see from the chart below that the 4050 support level is important, as hardly any volume (on left side of the chart) traded in the next 100 points lower. Meaning: If that support gives way, price could fall quickly and the index could revisit the 3900s, which would be a significant correction.

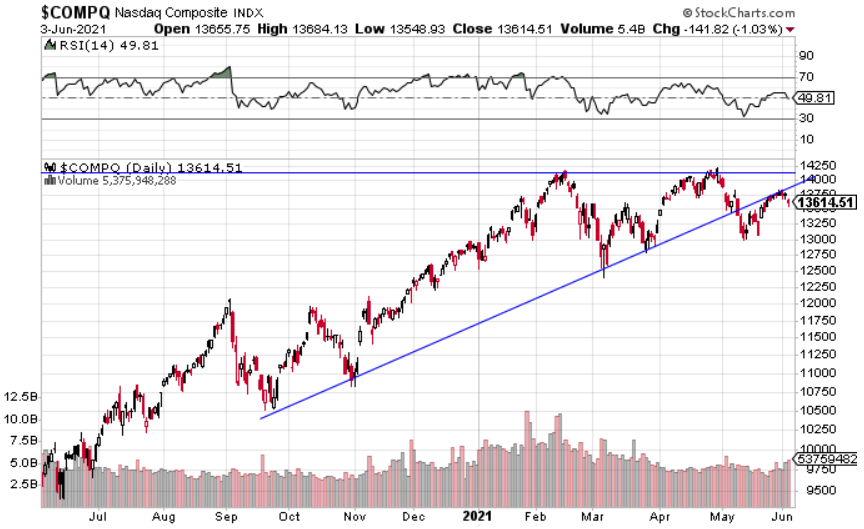

Although we like technology long term, the intermediate term price action continues to be weak. Updating our Nasdaq chart from last month we see more weakness as price is now trading below the uptrend line.

On a more positive note, the inflation and cyclically sensitive materials sector continues to charge higher. On a relative basis, this sector is one of the market leaders. If economic and inflationary numbers continue to rise, this sector will continue to lead.

The Federal Reserve continues to remain accommodating with emergency-level treasury bill purchases, or quantitative easing. The Fed has stated that any rise in inflation (as measured by CPI) will be short lived, and has maintained that interest rates will remain low through 2023.

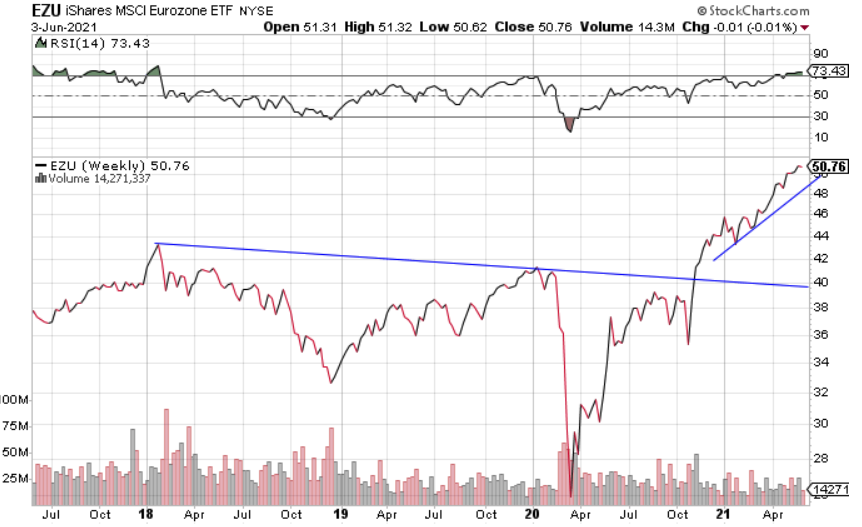

Global Equity: Europe Finally Picking Up Steam

We’ve spent most of our time covering emerging markets as they were some of the first countries to recover from the COVID-19 crisis and thus offered earlier returns on their equities. Europe, by contrast, has had one of the slowest responses to the pandemic. European countries consequently lagged in economic recovery. This lag may provide investors a safe haven over the next few months and quarters. As other countries have entered or started to enter the recovery exhaustion phase, Europe is closer to the beginning phases of recovery than the end. Although long term, Europe doesn’t have a particularly compelling story from a growth perspective, the short to mid-term may provide investors a great place to invest their money.

Real Estate: Technically, Perfect

Despite reaching new all-time highs last month, we called out the need for real estate to cool off in order to go higher. From a technical perspective, that call couldn’t have gone better. Price broke the trendline and corrected back to prior all time highs ($95) and rallied out from there. Real estate is now outperforming the stock market and up nearly 23% year to date.

Commodities: Rising Inflation Supports Commodities

Commodities spent May consolidating after hitting our $27 price target. The consumer price index (CPI) covering May data came in at 5.0% higher than the prior year. This was the highest print in more than two decades and was the boost commodities needed to take on new one-year high prices. Inflation will be very interesting to watch over the coming months. Currently, our outlook is that inflation is on the verge of peaking and could decelerate in the back half of the year, despite being higher than the 2% norm. However, the cost of goods producers use are still climbing, suggesting demand imbalances still exist ahead. Not to mention that if consumers fear inflation, they may pull forward purchases, accelerating trends higher. The next few months will be important to watch as key investment themes for 2021 will change as inflation does.

Fixed Income: Is the Bond Market Ignoring Inflation?

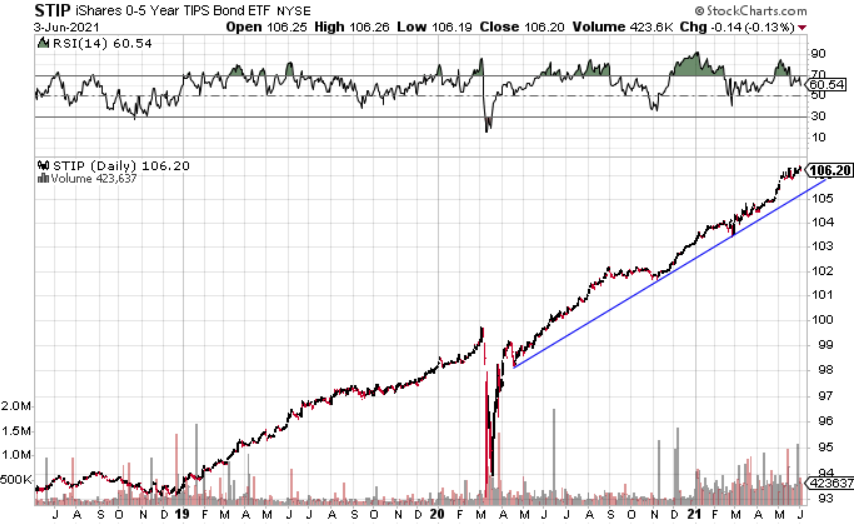

Interest rates continue to consolidate as the next move, up or down, seems to be nearing. Looking at the bellwether 10-year U.S. treasury rate on a short-term horizon, we can see the 1.60% rate has been stuck in the mud for nearly a quarter. This is in contrast with the recent inflation rate of 5%, putting real yields (nominal yields minus inflation) at -3.4%. That negative real yield leaves investors with limited options in the fixed income space.

Of the options, short-term inflation protected treasury bonds look the best. With shorter term yields just 0.3% and inflation at 5%, the premium from the inflation protection has guided these bond values higher for more than a year as short term rates have remained very low.

All Terrain Portfolio Update

The All Terrain Portfolio continues to rotate risk into the strongest performing assets within broader sectors. With many economic forces approaching key metrics, we continue to broaden our investment allocation. We will continue to follow our methodology and indicators to find buying opportunities and manage risk.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply