In a Nutshell: In an extremely rare event, both U.S. stocks and bonds fell in tandem this past month. Emerging markets finally broke out and the dollar continues to influence multiple markets.

Domestic Equity: Stocks Fall, Regime Change On the Way?

U.S. stocks fell in October in what is traditionally a weak month for stocks, and especially weak during election years. In fact, all of the last four election years, the month of October has seen losses averaging about -6%. The good news for stockholders is that in election years stocks typically finish the year higher from October.

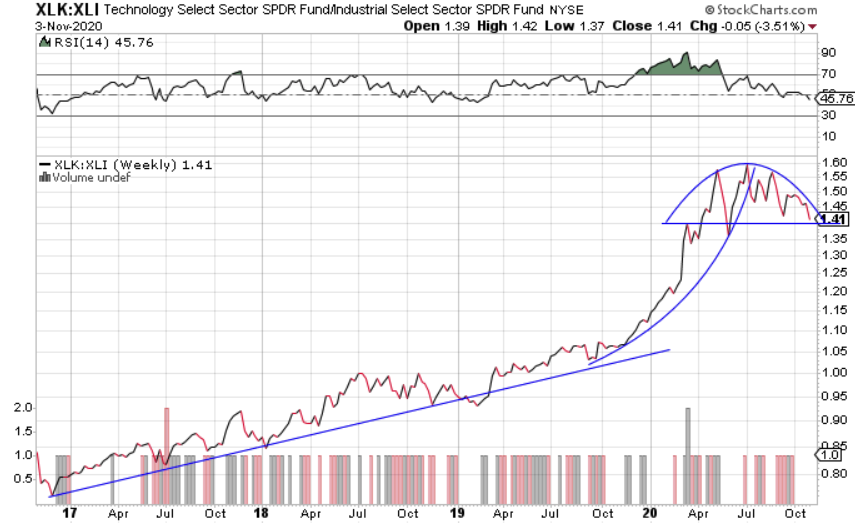

Technology has been a leader for stocks over the last few years, and dominated over the last year or so. But is tech ready to hand off its leadership status? Below is a chart showing the relationship of technology to industrial stocks. When this chart is moving higher, tech is leading, when lower, industrials are leading. Below, the dome-like shape shows a potential reversal in this tech leadership. With all the talk of fiscal stimulus, perhaps more cyclical stocks could take over and start to outperform technology. The path forward will be important not only for investor positioning, but future economic growth as well.

The Federal Reserve did not meet in October. Interest rates are still priced at 0% for the next 12 months. Lately, the Fed has put pressure on Congress to pursue fiscal spending in order to continue economic recovery out of the COVID-19 shutdown.

Global Equity: Breakout Complete

Emerging markets (EM) had a good month in October and finally broke out of a years-long consolidation. EM broke though the top diagonal line (below) and are now in the process of confirming the breakout. Seeing price fallback down to the trendline, and then moving higher, would indicate the breakout is complete. Emerging markets have performed well as of late, with Asia doing the heavy lifting. Many Asian countries have significant technology exposure though semiconductor production. If technology stays hot and the dollar continues to weaken, EMs will be very investor friendly.

Real Estate: Still Not Going Anywhere.

Real estate had a down month in October and still seems to be stuck between medium-term resistance and long-term support. On a relative basis, real estate is still lagging behind the broader market significantly. It seems real estate will be stuck in neutral until some sort of government stimulus package is decided on and includes commercial real estate.

Commodities: The Dollar Is Still Trying to Decide

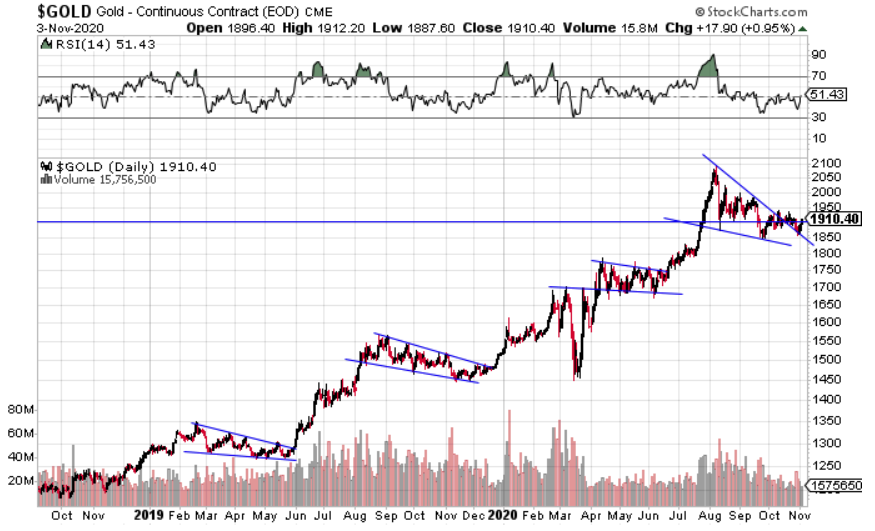

Our dollar chart below still indicates that it’s in charge of markets right now. You can see below the lowest point for the dollar over the last few months coincided with all-time highs in U.S. equity and gold prices. This relationship seems to be related to potential fiscal stimulus that Congress is negotiating on. More stimulus likely devalues the dollar and pushes stocks and gold up.

Gold is taking its time but seems like it is ready to come out of its months-long consolidation. Gold is now above the falling wedge consolidation highlighted below and looks ready to resume its trend higher. As stated above, gold could get a boost from a fiscal stimulus package agreement.

Fixed Income: Strange Times for Bonds

Bond markets are generally negatively correlated to equity markets. That is, when stocks go up, rates rise with stocks pushing bond prices lower. However, in October bond prices fell with stocks, offering no downside protection to traditional buy and hold portfolios. In fact, the last week of October was just the 17th week since 1962 where the S&P500 traded down with the 10-year U.S. Treasury rate increasing. On top of this recent oddity, the 10-year U.S. Treasury is now attempting to make a new six-month high. This dislocation and upward movement may be related to anticipated fiscal stimulus, but given the mean reversion potential in the chart below and the potential for a gridlocked Congress, rates could fall from here.

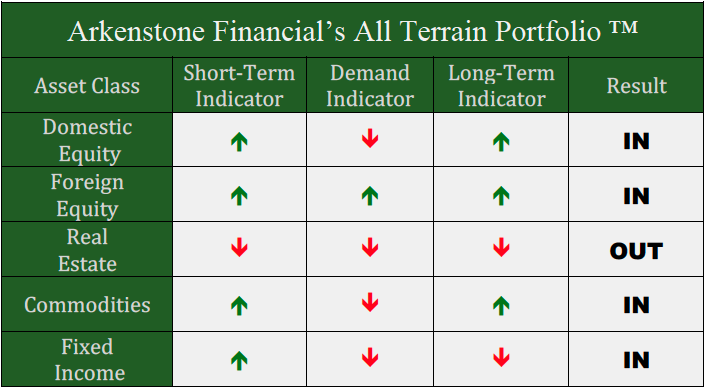

All Terrain Portfolio Update

The All Terrain Portfolio has maintained its risk exposure, but made some subtle changes to absorb increases in market volatility due to rising policy and political risk. However, we will look to add additional risk assets small in size and narrow in focus as opportunities are presented. We will continue to follow our methodology and indicators to find buying opportunities and manage risk.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply