In a Nutshell: Stocks, both global and domestic, along with precious metals, pull back because of recent dollar strength. All investor eyes are now on our next COVID-19 relief stimulus package.

Domestic Equity: Can Tech Keep Leading?

We suggested last month that U.S. stocks were ripe for a pull back and the Nasdaq promptly saw a 14% drawdown — a much needed cool off if we are to have a healthy and sustained bull market going forward. Even with this brisk pullback the Nasdaq still sits atop the long-term channel and is on a knife’s edge. An up move from here could solidify the “channel jump” idea, and that we are ready to go higher and at a higher rate. The flip side shows a potentially significant reversal pattern that, if completed, will take us back to the middle of the channel. Politics rarely drive the markets, but if U.S. politicians can come to an agreement on another large stimulus COVID-19 relief package, that would likely be the catalyst to take stocks higher from this elevated position.

The Federal Reserve spent the last month saying they will not raise interest rates from zero until 2023 and that more policy response is needed for the economy to recover. Additionally, the Fed members have been incredibly outspoken that Congress needs to pass a fiscal stimulus package (that the Fed would fund with more money printing) in order for our economy to have a chance at full recovery. Since the Fed is what saved stocks in the March sell off earlier this year, the fact that they have passed the baton to our politicians explains why all eyes are on Washington now.

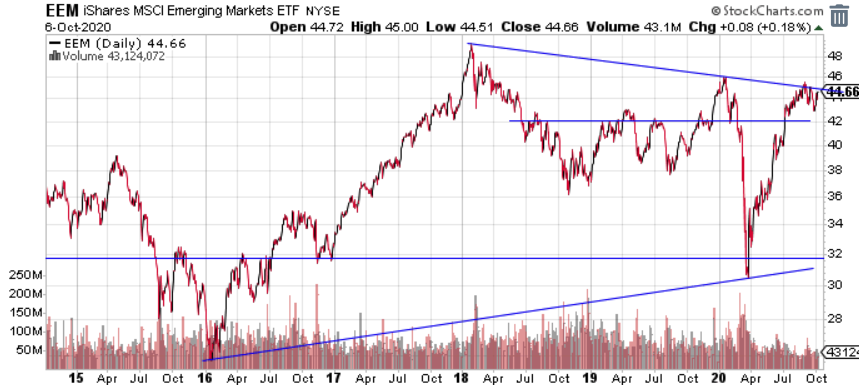

Global Equity: Fourth Time’s the Charm?

Emerging markets (EM) continue to struggle in breaking through resistance as highlighted by the top diagonal line below. After three major failed attempts over the last two years and three failed smaller attempts in the last three months, EMs look ready to break out. A break out from a consolidation this large will likely have a long life if it happens. A large long-term bull market could develop as a result. A strong dollar likely prevents this breakout from happening. A large stimulus package passed in the U.S. could weaken the dollar enough to send EMs sailing.

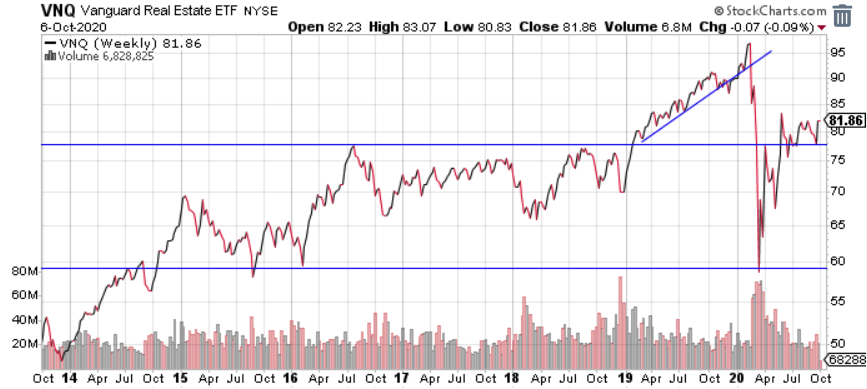

Real Estate: Still Waiting for a Move

The real estate sector was flat on the month and still trading about 15% below highs made earlier in 2020. Real estate continues to be without a clear path forward. Certain mortgages have had forbearance extended until early 2021 and many commercial real estate buildings are still not able to collect full lease payments from tenants. Real estate continues to be the forgotten sector of the U.S. economy when it comes to bailouts and stimulus. Maybe this next round of stimulus will give real estate the boost it needs.

Commodities: Everything Hinges on the Dollar

The U.S. dollar had a very strong month and looks to have completed a reversal out of its downtrend as described last month. In our view, the dollar’s path forward may have the most wide-ranging impact of any asset. A rising dollar would likely mean a new COVID-19 relief stimulus package was not passed and likely puts pressure on precious metals, U.S. stocks, foreign stocks, and interest rates. A significant stimulus package passed in Washington D.C. likely devalues the dollar and allows all of the aforementioned assets to rise. These types of correlated asset class scenarios put investors in a boom or bust situation.

Gold pulled back in September as rates and the dollar rose. Although gold slipped below the $1900 level we were looking for it to hold, the longer-term bull case remains intact. The current consolidation may take another month or two before breaking out, and could fall further between now and then. However, a breakout to the top of this falling wedge still has massive potential.

Fixed Income: Rates Breaking Out?

Bond markets typically do a really good job of telegraphing the next move for equities in advance. Though recent Federal Reserve intervention in the U.S. treasury markets can distort bond market signals temporarily, it seems now we have a relatively clear view. If this range-bound interest rate action (below) that we’ve seen over the last six months continues, then we should expect mean reversion back to the 0.6% range on the 10-year note and stocks likely falling along with it. If we finally breakout to the upside of the range shown below, stocks are likely rallying along with it. Looks like make or break time for interest rates and, potentially, stocks.

All Terrain Portfolio Update

The All Terrain Portfolio has maintained its risk exposure, but made some subtle changes to absorb increases in market volatility due to rising policy and political risk. However, we will look to add additional risk assets small in size and narrow in focus as opportunities are presented. We will continue to follow our methodology and indicators to find buying opportunities and manage risk.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply