In a Nutshell: Gold maintains its impressive run. Interest rates remain low and U.S stocks continue their Dr. Jekyll and Mr. Hyde rally.

Domestic Equity: In Tech We Trust

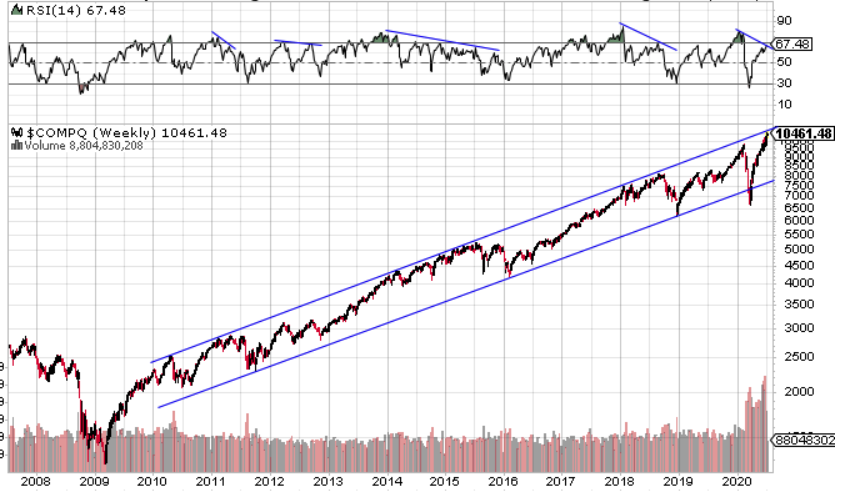

The U.S. stock market was mostly flat for the month of June, but expanded the gap between the haves (technology) and the have nots (cyclical sectors). We were looking for a healthy rotation from the leaders and into the laggards for signs of broader market strength. Unfortunately, in June we saw cyclical sectors like industrials and financials pull back only to see technology pull further ahead, making new all time highs in the process. The chart of the tech-heavy Nasdaq index is one of the most important charts to follow right now. The Nasdaq has largely traded within the channel illustrated below for over a decade. When the Nasdaq trades at the top end of the channel, over the medium term, risk is elevated and future returns are low – especially when momentum (RSI, top chart) is falling. When the Nasdaq is trading toward the low end of the channel, the risk/reward ratio is heavily tilted toward reward. It would not be appropriate to use this chart to conclude that a pullback is going to happen soon – though that’s always possible. This chart simply tells us that if this trend continues, there should be a better buying opportunity for tech stocks in the future when compared to current levels.

So what happened to the rotation into cyclical stocks? Sectors like industrials (below) tried to break out at the beginning of the month only to fail to hold the move and ultimately close the month lower – a story you’ll see in other sectors below.

The Federal Reserve kept interest rates pinned at zero in June and telegraphed that they would likely keep rates at zero through 2021. The bond market is pricing in zero rates though March of 2021 at a nearly 100% probability, with a small chance assigned to negative interest rates.

Global Equity: Steady Progress

Emerging markets (EM) was nearly unchanged for the month of June. A cool off or pause after solid rebound is likely a good thing for EMs. The top diagonal line is the real litmus test for EMs if we are really looking at a global economic recovery. EMs have not made a new high in over two years. If we break through this top diagonal line, the probability of a real recovery increases. Below this line, recovery may be further off than we’d like.

Real Estate: Still Lagging, Lacking Direction

Real estate was flat for the month of June, while whipsawing around a very important level. Last month we highlighted how the top horizontal line (below) was the resistance level for most of the last few years. We continue to see price action around this important resistance/support level. Simply put, any price action sustained above this top horizontal line would be good, and any price action sustained below this level would be bad for real estate. This may take a while to shake out, but the line in the sand has been drawn.

Commodities: Breakout 3.0 in Gold

Gold stayed on script in June and broke out of its third major consolidation in the last two years. Gold did exactly what we explained it would do in order to sustain the current bull market. Gold continued its consolidation and briefly tapped the low end of the short term range of 1675, then broke out through the top side of the consolidation. If the bull market case continues for gold and previous consolidations are any indication, we could see another $150-200 rally over the coming months. A rally of that size could take gold to new all time highs. Gold has not seen a new high in over a decade. The 1800 and 1900 levels could provide some resistance, but hopefully just temporarily.

Fixed Income: Breakout or Fakeout?

Interest rates tell a better story about the economy than stocks do. This is why we follow fixed income markets so closely. Interest rates tend to rise in periods of prosperity or recovery and fall in times of economic contraction. The chart below highlights the latter as the 10-year U.S. treasury interest rate fell nearly 70% in the first three months of this year. As we mentioned last month, the sustainability of our recent stock market rally would be increased dramatically if interest rates could rise with it. Since then we saw a huge spike in rates out of a consolidation. From that high point for rates in early June, rates have pulled back significantly and are now on the wrong side of a trendline. Meaning, if medium to long term interest rates seem inclined to stay flat or even fall further, as the chart suggests, that is not a positive economic sign.

All Terrain Portfolio Update

The All Terrain Portfolio will maintain its current risk level – albeit limited. However, we continue to look to add risk assets small in size and narrow in focus. We will continue to follow our methodology and indicators to find buying opportunities.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply