In a Nutshell: Stocks continue to ride the wave of liquidity provided by central banks around the globe. Gold takes off again with the U.S. dollar in limbo.

Domestic Equity: Stocks Love Liquidity

U.S. stocks finished a strong year with a strong finish. The positive price action in the S&P 500 coincided with low-to-flat sales and earnings growth. As a result, fundamental valuations for the S&P 500 show it to be expensive by historical standards. However, that doesn’t mean prices can’t continue to rise. As the past few decades have shown us, liquidity may be the most important factor in driving stock prices. With ample liquidity now being provided by the Federal Reserve though repurchase facilities, the markets seem content. With these liquidity injections set to end by February, the focus will likely be back on fundamental and economic data.

As mentioned previously, the Federal Reserve continues to provide funding relief to banks on a short-term basis. This funding will continue, but the Fed has not announced its intentions beyond January. Bond markets are currently pricing in flat future interest rate expectations, with the highest probability outcome of one interest rate cut in 2020. The only near-certainty markets are pricing in for interest rates is that they will not go up.

Global Equity: Emerging Markets Look Serious This Time

Emerging markets have been lagging foreign developed and U.S. stocks for the last couple of years, and still are nowhere near their 2018 highs. However, recently they have been making new relative highs as well as new 52-week highs. The horizontal line below highlights what appears to be a good test for emerging markets. We should expect a continuation of the current uptrend if emerging markets can stay above that support level.

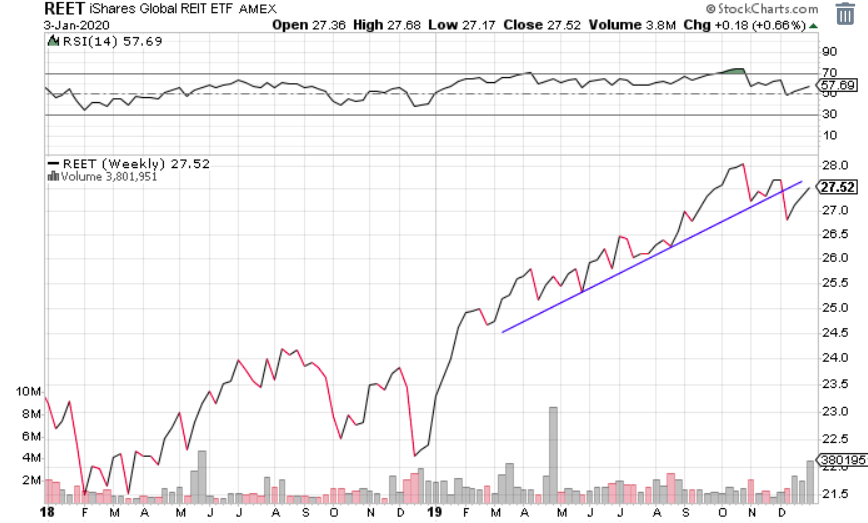

Real Estate: Has the Rotation Started?

Real Estate was one of the best performing asset classes in 2019. Due to the defensive nature of real estate, investors looking for return or yield flocked into real estate as recession fears grew throughout the year. As you can see below, the uptrend that was sustained all through last year has been broken. Given the “risk on” mentality of the current stock market, we may be witnessing defensive sectors falling out of favor. This doesn’t mean real estate will fall into a downtrend, but at the very least we’ll see a period of underperformance relative to stocks.

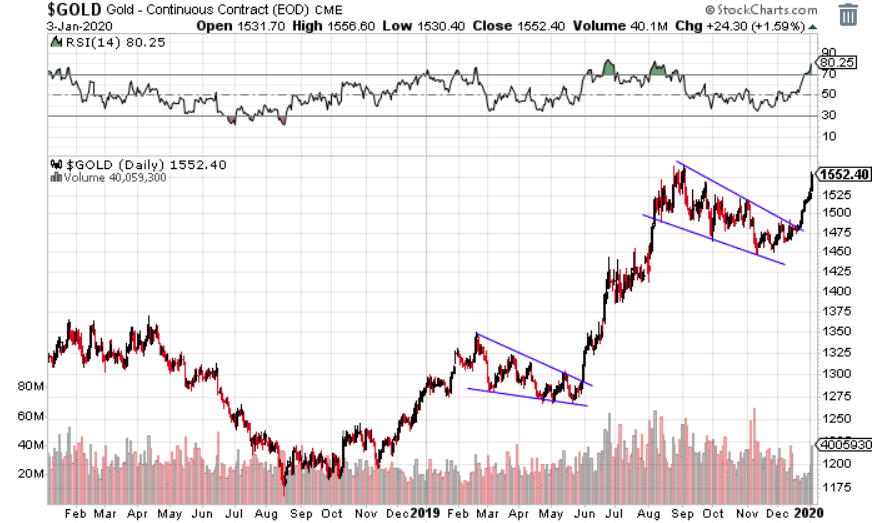

Commodities: Gold Pops Again, Dollar Weakening

Gold sprinted to the finish line in 2019, with a massive year-end rally. We suggested a move like this could play out as we observed a countertrend consolidation pattern within the context of a broader uptrend. The resolution of this type of consolidation often produces powerful upward moves, and we see just that below. Gold investors will want to see prices find support above the previous 52-week high from last September for further confirmation of this bull market in gold.

Gold has quite a few tailwinds right now, one of them being the weakening of the U.S. dollar. Over the last six months the Federal Reserve has done just about everything it can to weaken the dollar though rate cuts and firing up the money printing press again. Hence, it would make sense that the dollar would take a breather. Below you’ll see the dollar breakdown from its trendline, but hold recent support (horizontal line). If price action remains above support, it is likely we’re seeing the dollar take a breather before moving higher. If it drops below the support line, the uptrend might be over.

Fixed Income: Investors Sending Mixed Signals

Although stocks have reacted very positively to the Federal Reserve injecting liquidity into financial markets, bonds have painted a cloudy picture. Future interest rates for long-dated bonds are typically heavily impacted by expected growth and inflation expectations. Inflation expectations are now on the rise. Growth expectations generally rise when the Fed provide additional liquidity into the markets. Thus, the consensus view is that interest rates will rise. Yet long term rates haven’t budged. As you can see below, long-term bond pricing is actually attempting to break higher, which can only happen with long term rates falling. Time will tell, but along with the U.S. dollar, the direction of interest rates will be a major market influencer in 2020.

All Terrain Portfolio Update

The All Terrain Portfolio is close to fully allocated at this time as our indicators continue to produce positive results. We’ll continue to watch the data and our indicators for important turning points early in 2020.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply