Stock markets in the United States and abroad had excellent returns in 2017. Bonds, both government and corporate continued to struggle given their low yields.

Domestic Equity

U.S. Markets finished the year off strong after the latest tax reform was passed in mid-December. Most major indices were up by 20% for the year and appear to be primed for a strong 2018 on the heels of this major tax reform.

The Federal Reserve, as expected, raised interest rates by one quarter of one percent in December. The minutes released by the Fed revealed they intend to raise rates three more times in 2018. Markets seem convinced by the Fed’s proclamation as two to three rate hikes are currently priced into the markets. The first anticipated hike of the new year looks to be in March.

Optimism for the U.S. stock market outlook in 2018 is high, given the projected boost in GDP from tax reform. The question that remains is how this fiscal policy interacts with the Fed’s monetary policy. In addition to rate hikes, the Fed is reducing their balance sheet in 2018, so the liquidity injections they have been providing the economy are set to stop. Markets are hopeful that tax reform can pick up the slack.

Global Equity

Global investors enjoyed an incredible year in 2017. Developed and emerging markets had one of their best years in a decade with developed global stocks realizing returns in excess of 25% for the year. The storyline to monitor in the upcoming year is how these global economies handle their monetary policy. Specifically, Europe will be interesting to watch because of their large global economic impact, but also since their monetary stimulus program is set to expire by fall of 2018. Investors have responded positively to the stimulus package so far. Will there be enough momentum to sustain growth without it?

Real Estate

Despite corporate real estate’s weak month in December, the coming calendar year leaves room for optimism. Real Estate Investment Trusts, or REITs, look to benefit from the tax reform passed this past month, making them an attractive investment going forward. This, coupled with traditionally high yields, has real estate investors looking for a good year in 2018.

Commodities

Commodities had a strong December to round out an otherwise lackluster year. The falling dollar and tax reform seemed to give commodities a boost to finish out the year. Gold was the headliner with a 5% gain in December to finish off a solid year for the yellow metal. It seems investors are looking to gold as the potential for inflation increases due to a weakening dollar and a stronger economy.

Fixed Income

Corporate bonds were flat again for the month of December and continued to pay out weak yields. Government bonds fell slightly to round out a poor year as low interest rates continue to plague fixed income investors.

The yield curve continued to invert in December as, paradoxically, short-term yields have risen, while long-term yields have fallen. Typically, this type of yield action occurs prior to recessions. However, some investors will say that with the Federal Reserve pumping up interest rates, this once clear indicator—the yield curve—may have become distorted. Regardless of your stance, when short-term notes pay out more than long-term notes, it represents a mispricing of risk. When risk is not properly priced, breaks can occur. This situation bears monitoring, to say the least.

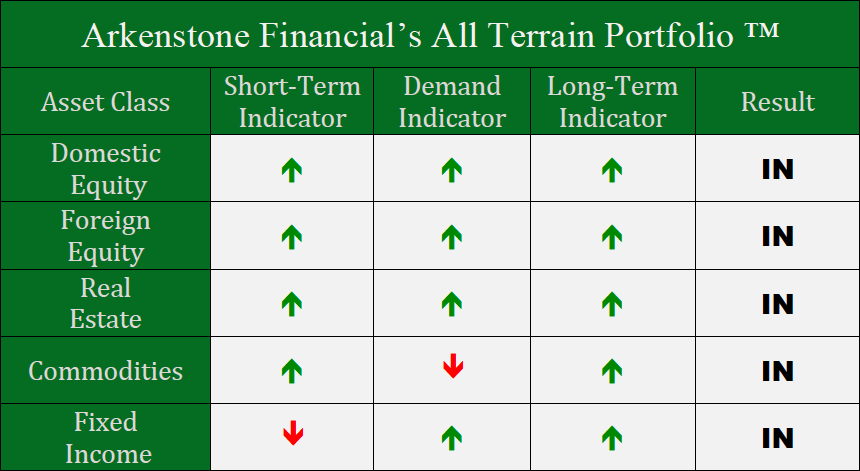

All Terrain Portfolio Update

The All Terrain Portfolio allocations remained steady in December. We will continue to follow our model closely and cautiously as a number of Central Banks across the global are approaching critical decisions in the upcoming calendar year.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

- Interest Rates Stabilize, Stocks Bounce - September 6, 2024

Leave a Reply