U.S and Global markets close out November on a high note as the odds of a U.S. corporate tax cut increase.

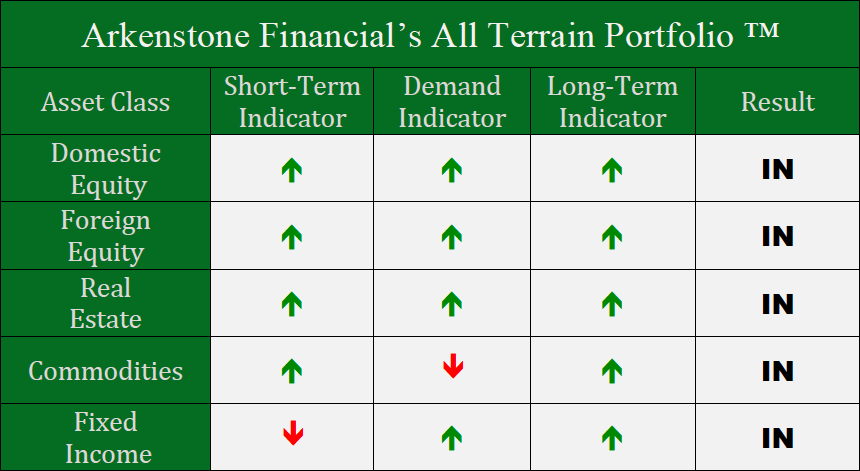

Domestic Equity

U.S. markets increased by 2.5% in November on the heels of tax policy momentum. The corporate tax cut bill has passed the House and looks to have the votes to clear the Senate in early December. Conventional wisdom suggests that a tax cut to corporations will increase profitability, and thus stock prices, pushing markets higher. However, since the election last November, U.S. markets have already gained about 20% in the anticipation of these corporate tax cuts. It remains to be seen if this rally will have much steam left after the policy goes into effect.

As mentioned last month, The Federal Reserve still looks intent on raising interest rates by 25 basis points, or 0.25%, on their upcoming December meeting. Currently markets have priced a 90.2% chance of a rate hike at that meeting.

The Fed is also on track to reduce their balance sheet starting in 2018. This would indicate (in addition to interest rate increases) the Federal Reserve is ready to “undo” some of the unprecedented monetary policy actions taken during the Great Recession. The question remains, will this reversal affect investors’ market sentiment and appetite for risk?

Global Equity

The European Central Bank plans to continue their monetary stimulus program, but pledged a gradual reduction over time.The head of the ECB, Mario Draghi, stated their version of quantitative easing will continue through September of 2018, but could continue past that if necessary. Simply put, investors have responded positively to central bank easing. This could provide for an interesting investment environment in 2018 with both the U.S. Fed and the ECB removing this monetary stimulus from markets.

Real Estate

The real estate investment market continued in its year-long holding pattern through November. The real estate proxy we follow has traded within a 4% range for all of 2017. Real estate has provided a nice source of yield for investors. With interest rates as low as they currently are, yield is hard to come by, making real estate attractive.

Commodities

Commodities was mostly flat for the month of November, but had a weak finish to the month. Despite the weak finish, technical charts would indicate they are still moving in broader upward trend.

Fixed Income

Corporate and government bonds were flat again for the month of November and continued to pay out weak yields. Low interest rates continue to plague fixed income investors.

The yield curve continued to invert in November as, paradoxically, short-term yields have risen, while long-term yields have fallen. Typically, this type of yield action occurs prior to recessions. However, with the federal reserve pumping up interest rates, this once clear indicator may have become distorted. We’ll continue to monitor this closely.

All Terrain Portfolio Update

The All Terrain Portfolio allocations remained steady in November. We will continue to follow our model closely and cautiously as December’s tax policy decisions may provide additional volatility.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply