As the Federal Reserve attempts to introduce tighter monetary policy, global and domestic markets now shift their attention to the possibility of U.S. corporate tax cuts.

Domestic Equity

U.S. stock markets have increased 15% to date in 2017. The more recent growth and push to record highs have been largely attributed to the hope of corporate tax cuts, a key initiative of the Trump administration. Although some tax cut details were released this week, the potential changes are far from a finished product. The Trump team hopes to have the bill passed by the end of the year. If the policy is adopted, the general perspective is that it will be a boon to large corporations and their investors alike, driving U.S. stocks higher.

As tax reform conversations heat up, the Federal Reserve attempts to cool down their accommodative monetary policies. The Fed is still looking to raise interest rates closer to historical norms. Their next chance to do so will be at their December meeting. Currently, markets have priced in a 96% chance that interest rates will be increased then.

Additionally, after nearly a decade of easy money policy, the Fed announced they will reverse course and begin reducing their balance sheet. For years after the Great Recession, the Federal Reserve has been injecting liquidity into the economy by buying U.S. Government bonds from banks. This created an enormous amount of debt on the Fed’s books. They will now attempt to offset that debt, albeit slowly, by selling those bonds back into the market place.

Lastly, President Trump has tabbed Jerome Powell to succeed Janet Yellen as Federal Reserve Chairperson. It’s expected for Powell to support the Fed policy put in place during Yellen’s tenure. The transition will take place in February of next year.

Global Equity

Foreign equities continue to have a fantastic year and are on pace for their best year since 2009. A big part of that success has been the European Union. The European Central Bank has declared they will continue their monetary stimulus program, but pledged a gradual reduction over time.The head of the ECB, Mario Draghi, stated their version of quantitative easing will continue through September of 2018, but could continue past that if necessary. As long as the ECB keeps their foot on the gas, European equities should continue to flourish.

Real Estate

The real estate investment market continues in it’s year-long holding pattern. Remarkably, a real estate proxy we follow has traded within a 4% range for all of 2017. We’ll continue to monitor closely as interest rate moves could affect this market.

Commodities

Commodities have been beaten up for years, but are finally starting to show signs of life. The stabilization in both the U.S. dollar and oil prices have given the broader basket of commodities some firm footing. Gold’s modest performance for the year has contributed to the attractiveness of commodities, as well.

Fixed Income

Corporate and government bonds were flat for the month of October and continued to pay out weak yields. Low interest rates continue to plague fixed income investors.

An item of concern in the fixed income market is yield curve inversion. Yield curve inversion occurs when interest rates in short-term treasuries rise while long-term treasuries fall. This type of movement can indicate a mispricing of risk. When risk is not properly priced, an economy’s health can be called into question. So far in 2017, the yield spread between a 10-year treasury and a 2-year treasury has been cut nearly in half. The anticipated December Fed rate increase may exacerbate this issue. We will continue monitoring this trend closely.

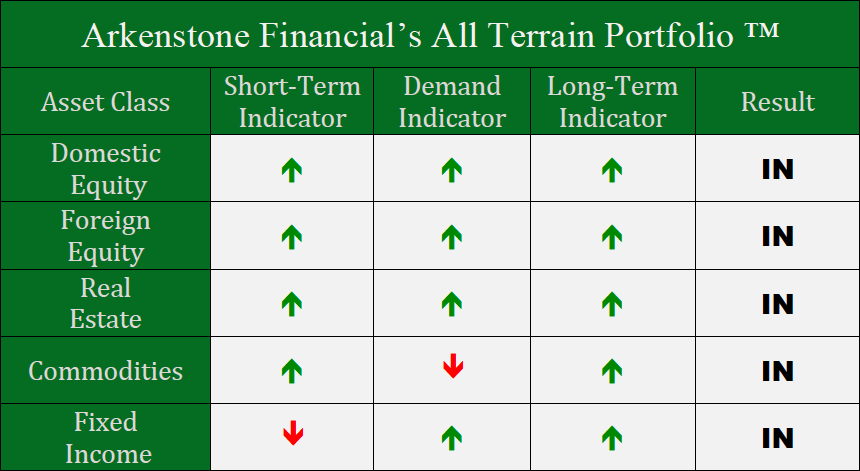

All Terrain Portfolio Update

The All Terrain Portfolio continued to show more green arrows in October, building off of mounting momentum over the last few months. We will continue to follow our model closely and cautiously as we near full investment within the model.

Past performance is not indicative of future results. Other asset classes or investment vehicles may be used in client portfolios and client portfolios may not hold all positions of the model at the same time as the model. This chart and its representations are only for use in correlation to the proprietary timing model by Arkenstone Financial, Registered Investment Advisor. Actual client and All Terrain Portfolio(TM) positions may differ from this representation.

- U.S. Stocks Make New Highs - December 6, 2024

- Rising Rates Create Headwinds - November 8, 2024

- The Fed Finally Cuts Rates - October 10, 2024

Leave a Reply